In his latest commentary about recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes the recent data on the Russian economy and notes that despite the general decline, the basic industries and defense sector are, in fact, showing positive dynamics. At the same time, the government supported the Finance Ministry’s proposal to freeze budget expenditures for the next 18 years, a move that will essentially scrap all the budget policies implemented by President Putin in the past.

(Left to right) head of Russia's Central Bank Elvira Nabiullina, Minister of Industry and Trade Denis Manturov, First Deputy Prime Minister Igor Shuvalov, President Vladimir Putin and Minister of Finance Anton Siluanov meet in the Kremlin to discuss the country's economic issues. Photo Mikhail Klimentyev / TASS

The Russian economy has hit bottom. Stagnation has arrived. Normally, even after a serious shock, an economy will find a new equilibrium and begin to grow again. Growth is normal for an economy, and decline is a reaction to crisis. But stagnation is an indication that something is wrong. Let’s hope we don’t have to wait long for growth to resume.

What Stagnation Looks Like

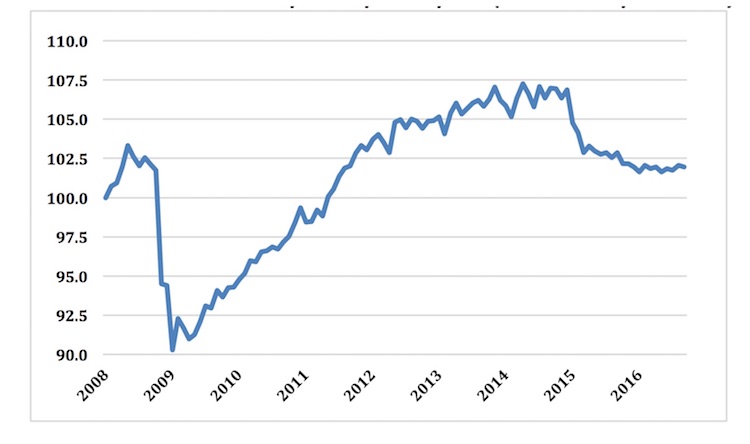

A good illustration of the condition of the Russian economy is the trend in the index of the VEB [Russian Development Bank], which shows early estimate of the GDP trend. I have already noted several times that the index lacks a steady trend: one month up, the next one down, two up, one down.

Chart 1. VEB Index. Recent valuation of GDP with seasonality and the calendar factor removed (100 = January 2008)

Source: VEB

To a considerable extent this can be explained by defects in the initial information released by Rosstat. How can you explain a growth of wholesale trade (which comprises 8 percent of Russian GDP) by 5 to 6 percent one month, and the next month, its fall by the same amount? The inability of Russian statistics to adequately measure the trends of even the most basic indicators became notorious long ago.

Change of Milestones

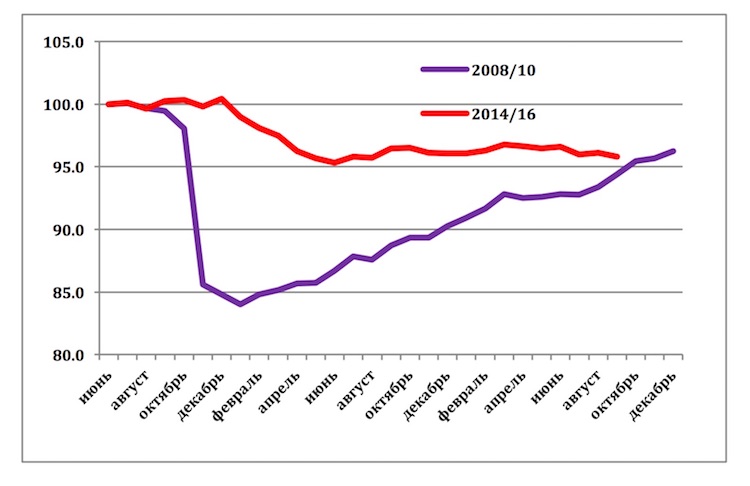

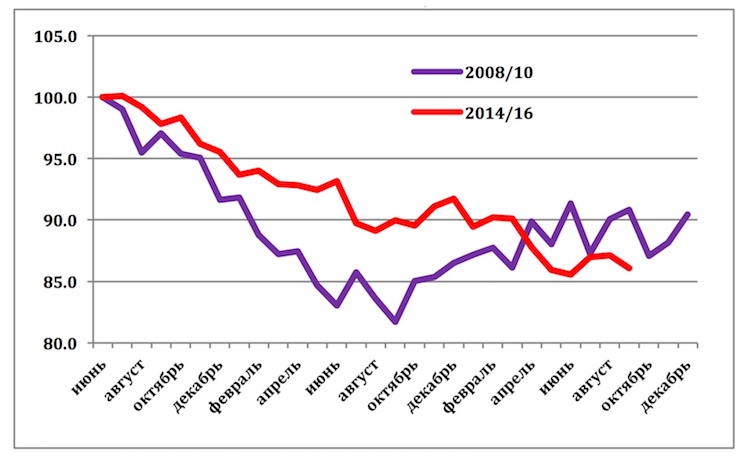

The instability of Russia’s economic trend, which is characteristic of stagnation, can also be observed on the level of basic indicators of production and consumption. What’s more, a peculiarity of recent months has been a “change of milestones.”

Right up until March of this year, many felt that Russian industry had begun, albeit slowly, to scramble up from the “bottom” onto which it had settled by last summer. But suddenly, beginning in April, the trend of industry as a whole became negative, and by the middle of autumn the level of industrial production was just a bit higher than the “bottom” of June 2015.

Chart 2. Trend of Russian industrial production, seasonally and calendar-adjusted, 2008–2010 and 2014–2016 (100 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development of the Higher School of Economics, National Research University. Months: June trough December of the following year.

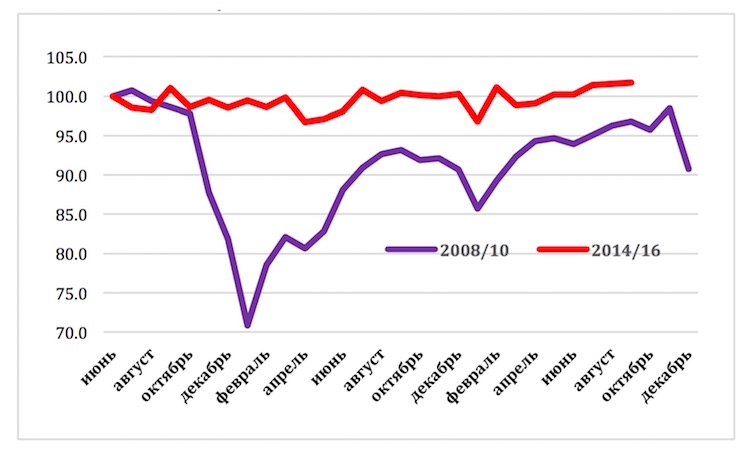

At the same time, the foundation of the Russian economy—the raw materials sector—is feeling quite confident. There’s no sign of external threat, such as a lessening of demand for raw materials in the world. A good illustration of this is the trend in rail freight turnover, more than 72 percent of whose strength is spent on the transport of raw materials and products of their primary processing.

So far the defense industry, which is generously financed from the budget, also seems to be doing okay. I don’t know if we can count on the rate of its growth to exceed 10 percent (as it has the last three years), notwithstanding the fact that formally the financing of defense sharply increased this year, because nearly all this growth has been for covering the credit scheme of arms purchases that was rolled out by the Finance Ministry in 2013–2015.

I will separately note that in the first place, military budget expenditures in 2013–2015 were understated, and in 2016, overstated. Secondly, the Finance Ministry permitted the banks to profit handily: Sberbank, VTB, Gazprombank, and VEB without any risk whatsoever provided credit to the arms industry at 10 percent interest per annum. Given that the scale of the credit scheme was about a trillion rubles with an average term for the credits of two years, the Finance Ministry ended up giving the banks 200 billion rubles. And the prime minister says there’s no money . . .

Chart 3. Trend of rail freight turnover seasonally and calendar-adjusted, 2008–2010 and 2014–2016 (100 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development of the Higher School of Economics, National Research University. Months: June trough December of the following year.

As for the industrial sector and its production of capital goods, its bad streak continues. A good illustration of this is the trend in construction, which continues to fall, although in housing construction the decline has already ended, and slow growth can be seen.

Chart 4. Trend in construction, seasonally and calendar-adjusted, 2008–2010 and 2014–2016 (100 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development of the Higher School of Economics, National Research University. Months: June trough December of the following year.

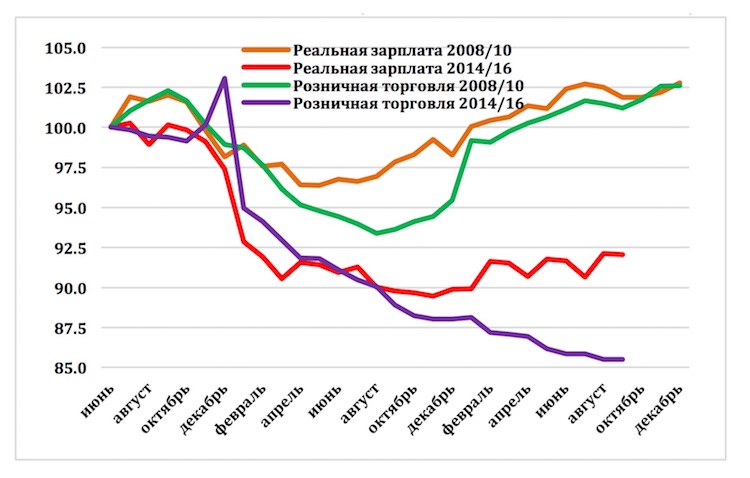

When I mentioned earlier a change of milestones taking place before our eyes, I was, of course, referring to the fact that, apparently, wages have begun to rise in the Russian economy (this can be seen in Chart 5, accounting for the wave-like movements whose nature is comprehensible only to Rosstat). As was the case following the crisis of 2008–2009, a growth in wages preceded a growth in public consumption. The lag at that time was five or six months, and this time, apparently, it will be one to two months longer. I’d at least like to believe that the worst is already over for the Russian population.

Chart 5. Trend of retail trade turnover and real wages, seasonally and calendar-adjusted, 2008–2010 and 2014–2016 (100 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development of the Higher School of Economics, National Research University. Months: June trough December of the following year. Orange: real wages in 2008/10; red: real wages in 2014/16; green: retail trade in 2008/10; purple: retail trade in 2014/16.

There Is a Proposal to Freeze the Budget

The government presented to the Duma a long-range forecast of budget policy up to 2034, which could end up being the tombstone for the budget policy President Putin has been carrying out in recent years.

Chart 6. Incomes and expenditures of the budget system in percentages of GDP (from 2006, accounting for non-budgetary funds)

Source: Ministry of Finance, Rosstat. Dark green: budget expenditures in the consolidated budget; light green: budget expenditures in the federal budget; red: budget incomes in the consolidated budget; orange: budget expenditures in the federal budget.

In this chart we see budget expenditures as a share of GDP. According to the forecast of the Economic Development Ministry, the realism of which we won’t get into, over 18 years GDP will grow at 1.6 percent per year, and thus the general volume of budget expenditures will grow slightly, although the share of budgetary expenditures in GDP will be reduced.

In the chart, which I borrowed from Vedomosti, beginning in 2000 a steady trend is visible in the growth of consolidated budgetary expenditures. True, this growth was not always even, but its trajectory over the last 17 years can be traced clearly.

In the budget forecast, the government supported the Finance Ministry’s proposal, which proposes freezing budget expenditures over the next 18 years. In real terms, this means that between now and 2034, corrected for inflation, consolidated budget expenditures, which are made up of federal, regional, and local budgets and non-budgetary funds, must grow by no more than 9 percent. In other words, 18 years from now budget expenditures will remain at practically the same level as this year’s.

I don’t understand at all how Russia’s existing social programs can fit into such a budget without raising the pension age and pension taxes or without lowering the real level of pensions. However, it’s obviously not worth waiting for economic growth support from the budget. And by growth support I don’t mean far-out proposals by adherents of soft monetary-budgetary policy, who consider it essential to pour hundreds of billions of rubles into the economy each year toward the realization of investment projects. I mean only necessary investment by the government in social and production infrastructure, which has been cut considerably during the last three years.

The Finance Ministry Doesn’t Need Money

So far, the Finance Ministry has not published data about the implementation of the budget in October, having declared only that not a ruble from the Reserve Fund was used that month. I can’t really understand why the budget department so stubbornly declines to finance planned expenses, moving the time for carrying out its promises closer and closer to the end of the year. But it’s clear that such a policy will have a severe impact on the monetary policy that the Bank of Russia is implementing.

The External Debt Is Almost Not a Problem

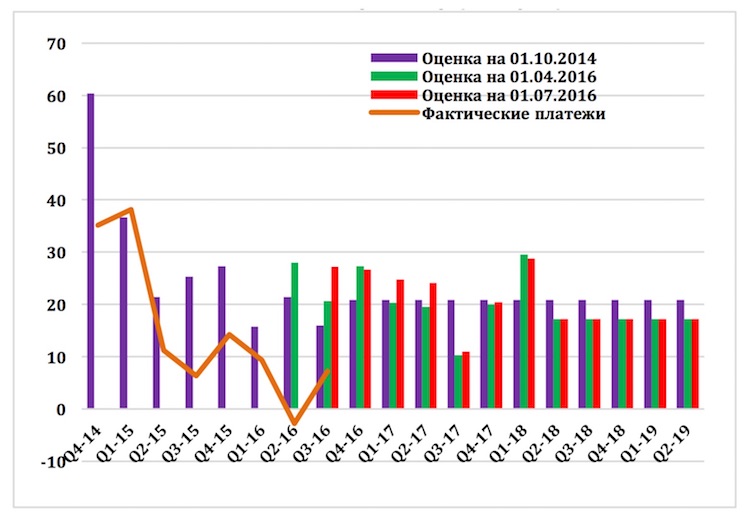

In the estimate of forthcoming payments on the foreign debt issued by the Bank of Russia, payments have been raised for the next four quarters, beginning with the already finished third quarter of this year. But I don’t see this as cause for alarm. For one thing, the forthcoming payments remain at a comfortable level for the Russian economy, at around $20 billion a quarter (including friendly credits), which is approximately two times lower than what we saw at the end of 2014 and beginning of 2015, when the currency crisis occurred. For another, Russian banks and companies that were not subject to the sanctions are more and more actively entering the market for foreign currency loans, which decreases the pressure of debt payments on the balance of payments. And the fact that a considerable part of the assets attracted are financed at the expense of domestic sources keeps us from seeing the full extent of these operations in the balance of payments.

Chart 7. Estimate of forthcoming payments on the foreign debt (billions of dollars)

Source: Bank of Russia. Purple: estimate for October 1, 2014; green: estimate for April 1, 2016; red: estimate for July 1, 2016; orange: de-facto payments.

What to Expect

The Bank of Russia has surprised no one with its decision to leave the key rate unchanged. Formally, there’s no reason to criticize the Central Bank: it was made clear in no uncertain terms that the issue of lowering the rate won’t be on the agenda until the first half of next year. Some wavering that occurred three weeks ago—speculation that maybe the rate could be lowered earlier, if oil were to get more expensive—came to nothing, as oil has, on the contrary, gotten 15 percent cheaper over the last two weeks.

But I said and I repeat: the Bank of Russia’s high rate does not influence monetary policy, as the Central Bank’s main instrument is quantitative restrictions. However, maintaining the rate at a high level sends a false signal to society, indicating that the monetary authorities are not confident about the stability of the achieved reduction in inflation.