In his latest commentary about recent developments in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes the reasons for the strengthening of the ruble, expresses cautious optimism concerning the automotive market, shows skepticism concerning the mortgage market, and once more notes the inconsistency of the actions of the Finance Ministry and the Russian Central Bank.

First Deputy Prime Minister Igor Shuvalov has recently announced that the government is planning the long-term stabilization of the ruble’s exchange rate. His statement came as a surprise at it contradicts the Central Bank’s proclaimed approach to a floating exchange rate. Photo: Alexander Shcherbak / TASS.

Nonresidents Strengthen the Ruble

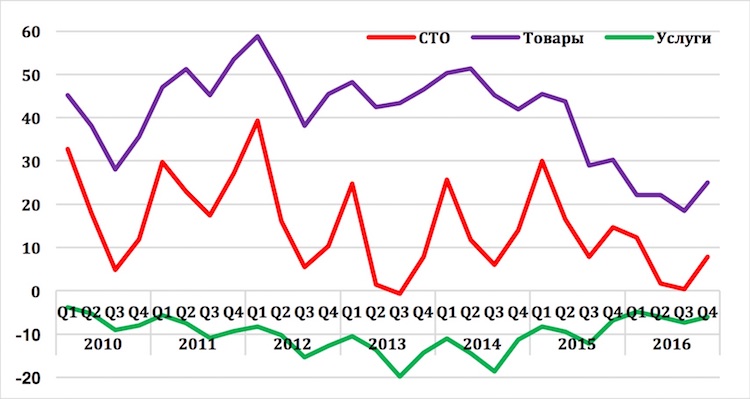

Despite growing oil prices throughout 2016, the stability of the Russia’s balance of payments (BOP) continued to weaken. The total value of Russian exports fell last year by more than 18 percent, with the export of petroleum products dropping by almost a quarter. Because the value of imports was in fact stable, this led to a lowering of the trade surplus by almost $61 billion, only one-fourth of which was compensated for by a lessening of the negative balance of services and wage payments. Overall, by the end of the year, the BOP decreased by almost two-thirds, from $69 billion to $22.2 billion, according to an estimate by the Bank of Russia.

Chart 1. Some components of the current account of Russia’s balance of payments (billions of dollars/quarter)

Source: Bank of Russia. Purple: current account; red: products; green: services.

Until detailed data are available, we can only hypothesize as to why, given such a weak BOP, the ruble’s exchange rate not only did not weaken, but even noticeably strengthened at the end of the year. My hypothesis is that the Russian ruble became one of the most attractive currencies for carry-trade speculators in 2016.

Thus, the value of federal loan bonds belonging to non-residents grew by 400 billion rubles during the first 10 months of last year (more recent data are not yet available). If we suppose that a similar sum was invested in other classes of assets (bank deposits, non-government bonds and notes, and shares), this would mean that during the year the flow of speculative capital into Russia was $13-15 billion.

Of course, this was a good thing for the stability of the ruble’s exchange rate in 2016, but every good thing must come to an end sooner or later. And what happens when this capital begins to leave Russia?

Bad, But Not Awful

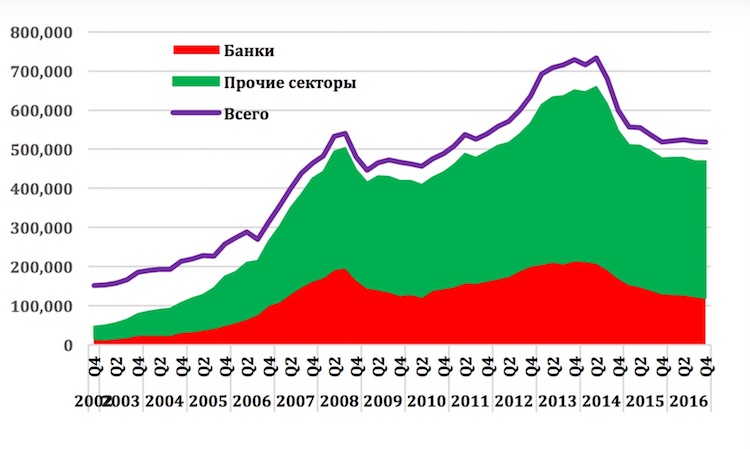

The Bank of Russia’s data about the trend of Russia’s foreign debt confidently tells us two things. First, reduction of the foreign debt (we are speaking about the cumulative debt of the government, financial, and corporate sectors) during the current crisis was much more painful than in the crisis of 2008-2009. This time it continued for six quarters, versus two previously, and the amount of foreign debt went down by almost 30 percent, versus 18 percent.

Second, the stabilization of the amount of debt in 2016 is evidence that the Russian economy managed to refinance 100 percent of the volume of repayment of foreign debt; in other words, the Western economic sanctions, although they remained in place, ceased to have a negative effect on the Russian economy.

Chart 2. Trend of foreign debt of the Russian Federation (billions of dollars)

Source: Bank of Russia. Red: banks; green: other sectors; purple: overall.

Cautious Optimism

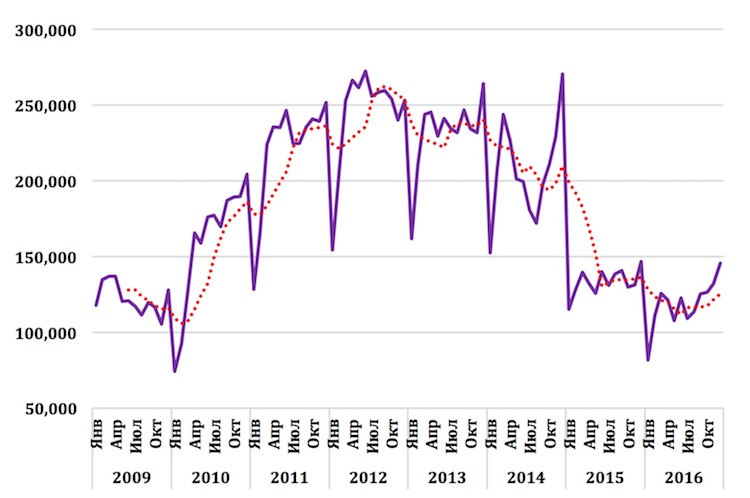

Seemingly, developments in the automotive market in 2016 were dismal: shrinkage of the market continued for a fourth year in a row; sales volume dropped 11 percent in comparison with the previous year; and each month last year (with the exception of November) showed worse results than a year prior. However, it seems to me that the year ended on an optimistic note. At least, in the second half of the year an upward trend took shape, and the market is much stronger than what we saw a year ago. If at the beginning of 2017 the automotive market is supported by a strengthening ruble, and if the price of oil doesn’t fall below $50 per barrel, then I think a turn in the market toward growth is guaranteed. However, we’ll wait and see.

Chart 3. Sales of new passenger cars in Russia, 2009-2016 (units per month and sliding 6-month average)

Source: Association of European Business

The Budget and the Central Bank’s Bet against Mortgages

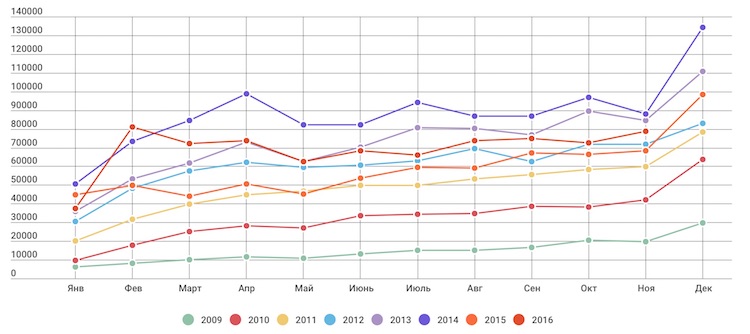

With regard to the mortgage credit market, I’ve yet to see any positive news. The number of new credits remained virtually stable over the year, as did the share of received credits intended to refinance old debt. It appears that if this segment of the market can be stimulated somehow, then a lowering of the key interest rate of the Bank of Russia or a broadening of programs for subsidizing interest rates out of federal budget funds could be the necessary means for such stimulus. However, while we can perhaps still hope for a lowering of the Bank of Russia’s rate, albeit not immediately, but over the course of two or three months, we can hardly hope for the subsidization of interest rates. The Finance Ministry decided to exclude these expenditures from the 2017 budget, and considering Russia’s continued strict approach to budget consolidation, we shouldn’t expect a restoration of this budget line. I am afraid housing construction in the coming year may unexpectedly have the wind knocked out of it.

Chart 4. Quantity of mortgage credits issued in Russia, 2010-2016 (units per month)

Source: Bank of Russia

Reserves Are Needed So They Can Be Saved

The 2017 budget year had scarcely begun when the Finance Ministry issued a statement that with the price of oil at $50 per barrel and the current exchange rate of the dollar at 60 rubles per dollar, the federal budget would receive approximately one trillion rubles of additional income, and if the price of oil were to rise to $55 per barrel, additional budget income could reach 1.4 trillion rubles.

However, no increase in budgetary expenditures is to be expected, and all additional income will be allocated to the replacement of the planned use of reserve fund assets. And so that no one doubts the firmness of this determination, Finance Minister Anton Siluanov immediately added that the decision had been confirmed by President Putin.

I can somewhat understand the president’s logic: although 2017 is a pre-election year, Putin is the obvious favorite in the race with no serious opponents and no chance of losing, so why cast pearls before swine and buy voters with additional infusions to the budget? Moreover, if suddenly the president’s support ratings were to fall, then nothing would stop him from hinting to the government that, well, it wouldn’t be such a bad thing to, for example, raise wages and pensions.

But the Finance Ministry’s logic is harder for me to understand. In essence, the budget has fallen into a closed vicious circle: a stagnating economy can’t generate a growth of budget income, and the desire to keep the remainder of the reserve funds’ assets untouched pushes the Finance Ministry toward a reduction of expenditures, which together with the ultra-high interest rate of the Bank of Russia lessens cumulative demand in the economy, which becomes bogged down deeper in the swamp of stagnation. How can we break free from this circle? The Finance Ministry remains silent, apparently shifting all responsibility to the Economic Ministry.

Is There a Way Out of the Vicious Circle?

At the Gaidar Forum, which was held in Moscow in January, I participated in the work of a round table on the topic “Strategy and Tactics of Monetary-credit Policy of the Central Bank of Russia.” Although neither the leadership of the Bank of Russia, nor the Finance Ministry, nor the Economic Ministry was present at this session, the discussion held with the participation of experts was quite interesting. During the course of it, I made the following observations:

- The Bank of Russia believes in the attainability of 4-percent inflation, but doesn’t want to lower it further, fearing deflation in certain commodity groups. The Bank of Russia cannot explain what the danger of such a situation is;

- Experts point out that a reduction of inflation in 2016 occurred in the context of a series of favorable market conditions, which might not be repeated in 2017, placing the goal of lessening inflation under threat. In the mid-term perspective, experts see the main risk befalling the labor market, where a revival in the economy could lead to a steady growth in wages;

- In response to my question about how to get out of the vicious circle, the director of the department of monetary policy of the Bank of Russia, Igor Dmitriev, agreed that the current interest-rate policy of the Central Bank is super-strict due to a desire to firmly tamp down inflation, and did not acknowledge the possibility of departing from such an approach. He also noted that an exit from the vicious circle is beyond the competency of the Finance Ministry and the Bank of Russia, and that it must be sought in the realm of “structural reforms, about which a great deal has been said at the forum.”

An Unexpected Statement

First Deputy Prime Minister Igor Shuvalov’s unexpected statement about the development of plans for the long-term stabilization of the ruble’s exchange rate came less than a week after the Gaidar Forum, where government bosses had an excellent opportunity to tell us about their plans and ideas. But since this wasn’t done, I’ve concluded that the government must have consciously decided to turn the Gaidar Forum into a “place where we don’t discuss things.”

Outwardly Shuvalov’s statement is totally at odds with the Central Bank’s proclaimed approach to a floating exchange rate for the ruble and contrary to promises to use currency intervention exclusively for the smoothing out of sharp market fluctuations in the exchange rate.

However, a year ago the Central Bank declared that it now had another goal: increasing foreign currency reserves to $500 billion. And this second goal came into clear conflict with the first: if the Bank of Russia buys up foreign currency on the market, then it counteracts the strengthening of the ruble’s exchange rate. In other words, it doesn’t give it free scope. In May–June of 2015, the Central Bank carried out a currency intervention when the price of oil was in the range of $60-65 per barrel and the dollar’s rate of exchange to the ruble dropped lower than 50. In other words, the bank has already shown that the freedom of the ruble’s exchange rate is permissible only within certain limits. Therefore, Shuvalov’s statement shouldn’t come as a surprise: although formally it contradicts the exchange rate policy of the Central Bank, it fully corresponds to the way the bank acts.