In his latest commentary about recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes the statistics for the third quarter and notes a slight upswing in the economy. However, the positive trend may be unstable, so it’s too soon to start talking about the end of the recession.

Sergey Aleskashenko is puzzled by the “stubborn reluctance” of Russia's Finance Ministry to even out peak budget expenditures at the end of the year (depicted above is the Finance Minister Anton Siluanov). Photo: Mikhail Klimentyev / TASS.

Up and Down, Repeat

Rosstat’s report that in the third quarter of this year Russia’s GDP was 0.4 percent lower than it was a year ago doesn’t tell us much about the condition of the economy in the larger scheme of things; Rosstat didn’t venture to say whether or not it has emerged from economic decline. All I can do is express, as I have countless times before, surprise over the fact that the country’s statistics department can’t just arrange for the release of information about GDP trends compared to the previous quarter. And also to repeat that for the Russian authorities, the absence of such data is tantamount to the absence of a working speedometer and compass when flying an airplane. (And I repeat that this situation has persisted since 2012).

This time our situation is made a little easier by the analytic centers, which unanimously point to the weak growth of the economy in the previous quarter. The Economic Ministry has identified a 0.1 to 0.2 percent growth, the VEB says 0.1 percent, and the Center for Development, 0.16 percent. Since no such unanimity has been seen before in experts’ evaluation of the economic trend, I propose to agree on the estimation that the Russian economy grew at the rate of 0.4 to 0.45 percent per annum.

It is impossible as of today to confidently answer the questions of how stable this growth will be, whether it will continue in the final quarter of the year, and whether we will be able to anticipate an end to the recession. For one thing, we must await more detailed data from Rosstat, which will show what accounted for the growth of the economy in the third quarter. For another, data about the trend of industrial production in October were not inspiring: -0.2 percent overall, including -0.7 percent in the extractive industries, which have grown over practically the entire period of the crisis. After the summer surge, the volume of new housing supply went down again (in October -13 percent compared to last year), and the decline in retail trade continues.

In short, everything looks exactly like it should during a recession—now up, now down, now better, now worse.

No Evenness

The stagnation of federal budget incomes comes as no surprise to many: if the economy is growing at all, it does so only symbolically; the price of oil refuses to go up as well. But the stubborn reluctance of the Finance Ministry to even out peak budget expenditures at the end of the year cannot but provoke a sense of surprise verging on incomprehension. In October (according to the latest accounting by the Treasury) budget expenditures were lower on average than they were for the previous nine months of the year.

As a result, the budget overhang reached such a size that in the event of full implementation of the budget for expenditures and the evenness of expenditures, in November and December the Finance Ministry must inject into the economy 77 percent more assets than in October. Understandably, such budgetary policy cannot but cause alarm at the Bank of Russia in expectation of what can happen on the currency market at the turn of December to January.

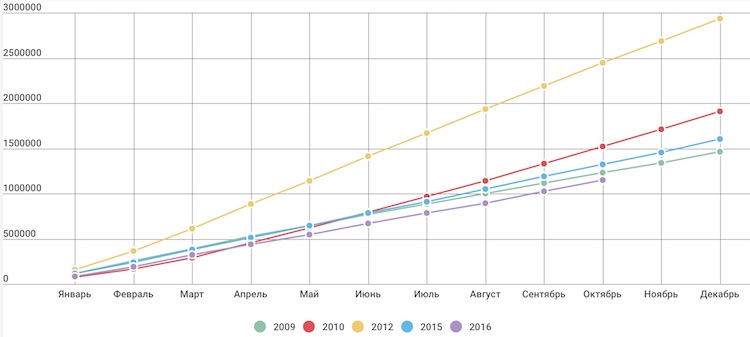

Little Chance of Seeing a Million and a Half in Car Sales

The October data about the sale of new passenger cars in Russia—down 2.5 percent compared to October a year ago—confirmed gloomy estimates of the condition of consumer demand. In order for the yearly sales volume to come out to one and a half million, sales in November and December would have to be 20 to 25 percent higher than in 2015. That hardly seems likely.

The good news is that in comparison with the end of 2009, when the economy had already obviously emerged from the crisis, the situation doesn’t look so bad—there have already been three months in a row when sales volumes have exceeded the corresponding levels from that year.

Chart 1. Sales of new automobiles in Russia, 2009–2016 (units, cumulative total from the beginning of the year)

Source: Association of European Business

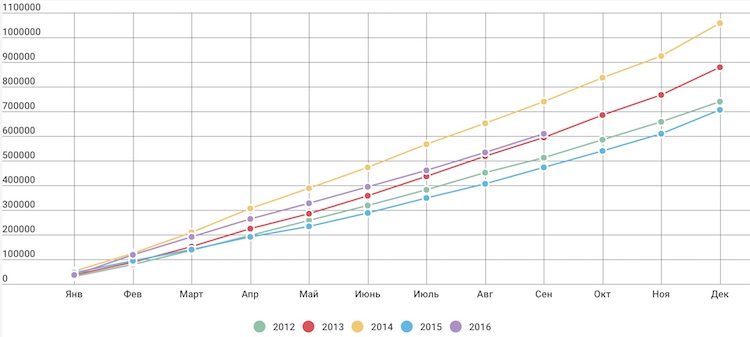

Housing is More Important than Cars

In comparison with the sales market for passenger cars, the market for mortgage credits doesn’t look so bad. The falloff in the quantity of credits issued is only 20 percent in comparison with the peak figure of 2013. While the acceleration the market experienced at the beginning of this year (+60 percent compared to the first months of 2015) has slowed, it has not disappeared completely. The quantity of mortgage credits issued in the last nine months of this year was 28.6 percent higher than last year’s level. As a result, it looks like summary data this year will turn out a little lower than the level for 2013, which in comparison with many other indicators is not bad at all.

Chart 2. Issuance of new mortgage credits in Russia, 2010–2016 (units, cumulative total from the beginning of the year)

Source: Bank of Russia

If in 2012 for every 100 newly sold automobiles there were 25 issued mortgage credits, this year the correlation reaches 60. Such a substantial difference in the trend of car sales and issuance of mortgage credits may indicate Russians’ long-term optimism: not ready to buy a new car under conditions of sharply falling incomes, they are willing to buy homes on credit, to all appearances counting on a more favorable long-term future.

Chart 3. Share of mortgage credits (quantity) intended for refinancing previously received credits

Source: Bank of Russia

Apparently, the only sign of a persistent crisis condition in the market for mortgage credits is the still-high level of the share of credits that are intended for refinancing previously received credits—more than 60 percent. In the pre-crisis period this indicator was in the range of 40 to 60 percent. By the way, under conditions of steadily, albeit slowly, falling mortgage interest rates, a high share of refinancing may be the new normal. This remains to be seen.

The Banking Sector is Shrinking, but Continues to Earn

The latest banking system development summary ratings for October, published by the Bank of Russia, were totally expected: banking activity is gradually shrinking. Since the beginning of the year (corrected for currency revaluation) the assets of Russian banks fell by 0.2 percent, the volume of credits furnished to the non-financial sector by 1.5 percent, and the volume of assets in the accounts of the non-financial sector by 5.3 percent.

Some optimism can be derived from the data about the growth in deposits by individuals (4.7 percent) and credits issued to them (0.9 percent), but this optimism dissipates if we remember that we are talking about nominal indicators, and that consumer inflation for ten months totaled 4.5 percent (or 5.2 percent in terms of base inflation). It turns out that the reduction in banking activity appears to be much more serious, down by about 5 percent in real terms.

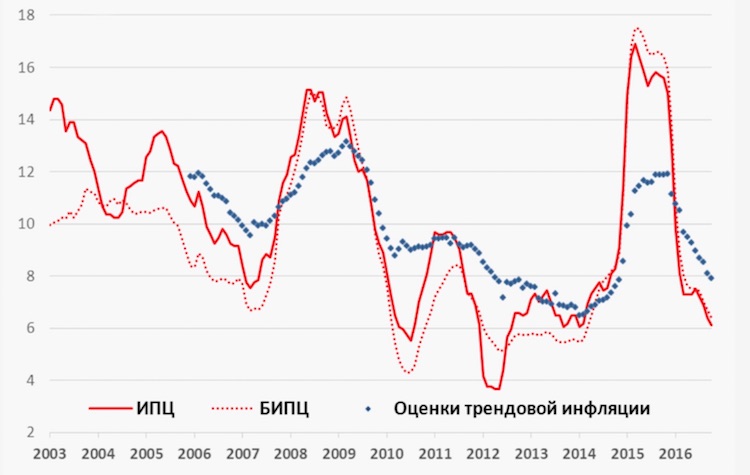

Chart 4. Tendency of consumer and trend inflation in Russia

Source: Bank of Russia. Red, solid: consumer price index (CPI); red, dotted: core CPI; blue, dotted: estimate of the trend inflation.

The reasons for this are well understood. For one thing, the Bank of Russia continues to carry out a super-strict monetary policy, keeping real interest rates (the difference between the key rate of the Bank of Russia and expected inflation in twelve months) on the level of 500 to 550 basis points, which makes credit unobtainable even for steadily working companies that are not connected with the export of raw materials. For another, the continuing cleaning out of the banking system inevitably influences the overall statistical data.

We can put two factors into the category of good news: 1) apparently, the growth of overdue bank balance debt has ended; and 2) the cumulative financial result of the activity of the Russian banking system over the last ten months (profit plus allocations to reserves) remained at last year’s level, while the volume of operations has shrunk.