Sergei Aleksashenko, nonresident senior fellow at the Brookings Institution and former deputy chairman of the Russian Central Bank, looks at the preliminary statistical data published by the country’s Federal Service of State Statistics (Rosstat), and notes that though officials try to downplay inflation growth, pessimism among Russian citizens is increasing. A deterioration of living standards is causing the country’s post-Crimea “patriotic enthusiasm” to wear off.

A graffiti project in St. Petersburg, Russia, depicting the falling Russian ruble. Photo: Peter Kovalev / TASS.

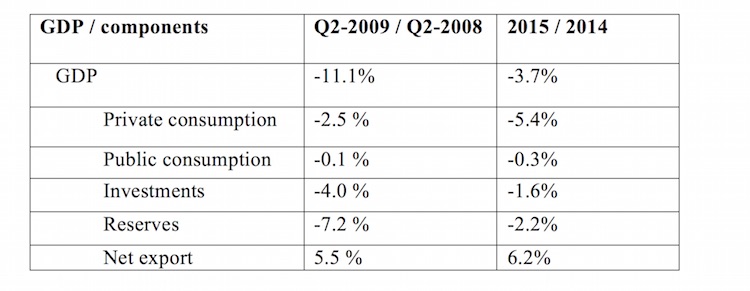

Rosstat published its first assessment of Russia’s GDP for 2015 and, as anticipated, the country’s economy contracted by 3.7 percent last year. The numbers do not reflect the quality of the change, though. The main cause for the contraction was a drop in domestic demand: its components accounted for a 9.6 percent decrease of GDP, which was compensated for by an increase in net export (or a decrease in imports).

Table 1. How components of domestic demand impact the GDP dynamics during crises

Sources: Rosstat, HSE Development Center

Compared to the 2008/2009 crisis, last year’s drop in private consumption was much more drastic—a decrease of 10 percent—while investments decreased only moderately—by 7.4 percent, compared to 19.4 percent in 2008/2009.

According to other official statistics by Rosstat, public demand in Russia dropped by only 1.8 percent during this same timeframe, while expenditures of the consolidated budget increased by 6 percent, with inflation being at 13 percent. I, for one, am skeptical of Rosstat’s current assessment of public demand dynamics.

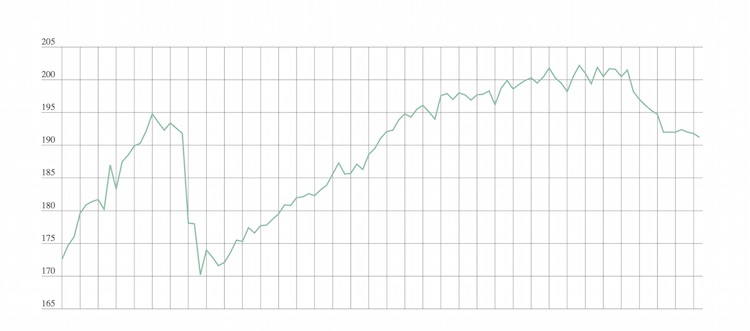

At the moment, there are two competing views on Russia’s 2015 fourth-quarter dynamics. Drawing from the dynamics of the country’s primary industries, the Development Center (a think tank based at the Higher School of Economics in Moscow) estimates that the economy grew slightly, while Vnesheconombank’s analysts, who produce their monthly estimates based on immediate data, have observed a slight decline. The implications of such a discrepancy are significant: if the Development Center’s estimates are correct, the Russian economy technically came out of recession in mid-2015 and afterwards grew two quarters in a row. If the truth lies with Vnesheconombank’s projections, the decline continues.

Chart 1. GDP Evaluation by Vnesheconombank (January 1999 = 100, excluding seasonal factors)

Source: Vnesheconombank

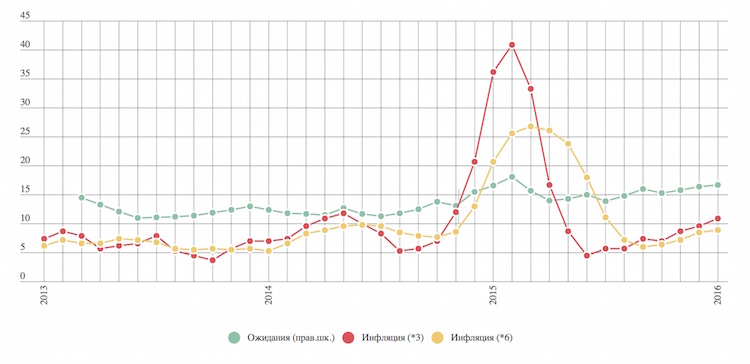

On the one hand, the unusually low inflation (1 percent) in January confirms the disappointing statistical data indicating a drastic decrease in demand and a deterioration of living standards. On the other hand, the chart 2 shows that after inflation dropped to its lowest level of the year last summer, it gradually started growing. Optimistic official reports based on 12-month floating inflation indicating that price growth is slowing down are products of the base effect—that last spring’s high inflation masks the latest trend. Today, price increase is higher than a 10-percent benchmark, which is a lot for an economy in which domestic demand is dramatically declining.

Additionally, the general public’s expectations for January 2016 inflation signal further price growth. This isn’t good news—not for the economy, nor the public, nor the Bank of Russia, which fails to manage these expectations.

Chart 2. Inflation in Russia (three-month and six-month) and the general public’s inflation expectations, 2013–2016 (%)

green – expectations; red – three-month inflation; yellow – six-month inflation.

Sources: Rosstat, Bank of Russia

The supervising authority of Russia’s Central Bank never fails to surprise me. The announcement by the bank’s deputy Chairman Mikhail Sukhov, stating that foreign assets would be subjected to reservation with a 10 percent premium compared to ruble assets, makes me think than the only aim behind this decision is forcing banks to sell their foreign-exchange holdings and switch to rubles despite any additional risks accepted by the banking system afterwards.

At the same time, it also makes me think that the oversight department of the Central Bank might have a different vision on the sustainability and profitability of the Russian banking sector—different from mine, which is based on information indicating that the banks are experiencing losses and receive constant support from the federal budget. Data from the last six years or more (at least since the 2008 crisis) has demonstrated that favoring the dollar didn’t create problems for banks. But the opposite stance—favoring the ruble—yielded contrary results.

Meanwhile, anti-crisis brainstorming within the Russian government has yielded unexpected results. It seems such efforts are being channeled toward finding ways to bring money to the federal budget—by any means. Over the last weeks there were several developments:

- Vladimir Putin supported the beginning of privatization; however, he insisted on so many preliminary conditions that, in my opinion, it would be impossible to sell anything if one was to follow all of them. Of course, I’m not talking about systemic privatization where the government pulls out of controlling the business (the president named keeping this control as his number one condition), but about selling minority stakes. Thus, the only goal of such privatization is financing the federal budget deficit;

- The Finance Ministry supported increasing excise duties for gasoline and diesel starting April 1, 2016;

- The Finance Ministry suggested introducing excise duties on “harmful goods” starting July 1, 2016. The list of such goods (except for palm oil) is yet unknown;

- The Finance Ministry suggested introducing excise duties on motor tires;

- Minister of Economic Development Aleksei Ulyukayev suggested passing “special measures” to “reap off… excessive foreign-exchange liabilities… from the banks,” or simply put—introducing compulsory state loans;

- Minister of Finance Anton Siluanov announced that if oil prices remain at their current level, he will insist on changing the formula that determines the crude export duty to increase pressure on oil producers.

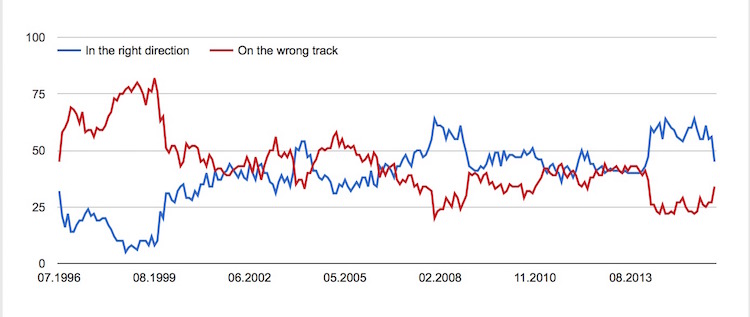

A survey published in January by the Levada Center, an independent Russian pollster, reveals a drastic drop in public approval of Russian authorities: approval ratings of the government, the State Duma, and governors have all gone down. The president’s approval rating has also decreased, albeit only slightly, and at the moment this drop is within the survey’s margin of error.

Chart 3. Survey: Is Russia moving in the right direction or is this course is a dead end?

Source: Levada Center

At the same time, it looks like public optimism about the country’s state of affairs has decreased. The number of “optimists” who think Russia is moving in the right direction and the number of “pessimists” who believe it’s heading toward a dead end are rapidly closing in on each other. It seems that Russia’s “post-Crimea enthusiasm” has started to wear off. Will there be a hangover?

It’s worth adding that it’s not just Russian authorities who are facing economic woes. There are signs of trouble in the United States as well. The latest data shows that wages are growing at rate of about 2.5 percent annually. This will soon lead to a higher rate of price increase. We can conclude that Federal Reserve System will finally be able to “boldly” raise its key rate.

This article originally appeared in Russian at openrussia.org.