In his latest commentary about recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes available Rosstat data for 2016 and concludes that, with the exception of a few industries (agriculture, fishery, extractive sector, electricity), the economy continues to decline.

On December 6, 2016 Elvira Nabiullina, chairwoman of the Bank of Russia, announced the decision to keep the key rate unchanged at 10 percent. Photo: Alexander Shcherbak / TASS.

Read the Classics

Rosstat’s recently published data on Russian GDP for the first three quarters of 2016 do not affirm the view of those observers who argue that the Russian economy has bottomed out. On a side note, I’d like to point out that so far the State Statistics Service hasn’t been able to resolve the trivial issue of adjusting its data for seasonal and calendar factors, which does not allow us to compare the current GDP dynamics to last year’s quarterly data and to determine how much various sectors contributed to the results of each quarter. Therefore, I can conduct analysis of the data for the last consecutive four quarters, but that does not shed light on what has been happening in the economy in the most recent months.

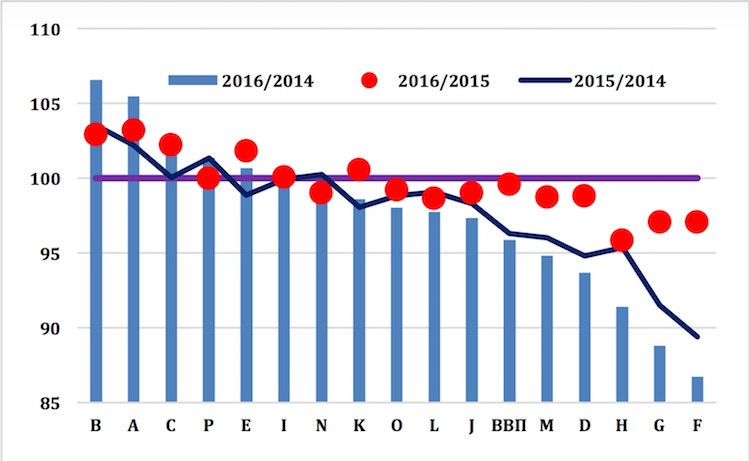

Chart 1: Russia’s GDP dynamic by sector (%%), Q3, 2016 over Q3, 2015*

Source: Rosstat

Chart 1 shows that various sectors of the Russian economy have been experiencing the current crisis in different ways. It seems that the crisis hasn’t really affected two sectors: agriculture and fishery. Both grew in 2015 and 2016. (Since we are only looking at the data for three quarters of each year, it’s the growth of Q3, 2015-2016 against Q3, 2014-2015.) The government has been constantly telling us about success in agriculture, but one has to do justice to Prime Minister Medvedev, who stated that the foundation for this success had been laid many years ago. Still, I was surprised to find out that fishery is now one of the “growth drivers”—especially since the problems in this industry were discussed so many times after Russia imposed its own counter-sanctions against Europe. But fishery’s achievements are clear: its export is rapidly growing. Or, in other words, it is growing for those focused not on the stagnating domestic market and decreasing household incomes, but on the growing consumption outside Russia and rip-off benefits resulting from the decreased costs following the ruble devaluation.

Last year, the extractive industry stagnated due to decreasing gas supply to Europe, but in 2016 it has recovered its lost positions:

- production (and export) of oil, gas, and coal has increased; coal especially benefited from a highly favorable pricing environment;

- generation and distribution of electricity, gas, and water have also grown and compensated for last year’s losses.

Growth in the real estate sector reversed the decline, but the small scale of this growth didn’t amount to a full recovery.

Meanwhile, all other industries continued to decline, thus leading to a very unpleasant change in the economy structure—the share of the basic materials sector expanded. And it comes as no surprise that the construction sector showed the worst performance, which reflects the ongoing decline in investment and public funding. Wholesale and retail performed just as badly as a result of the falling public consumption that canceled other positive trends altogether—improving foreign economic conditions, growing export revenues, and revived imports.

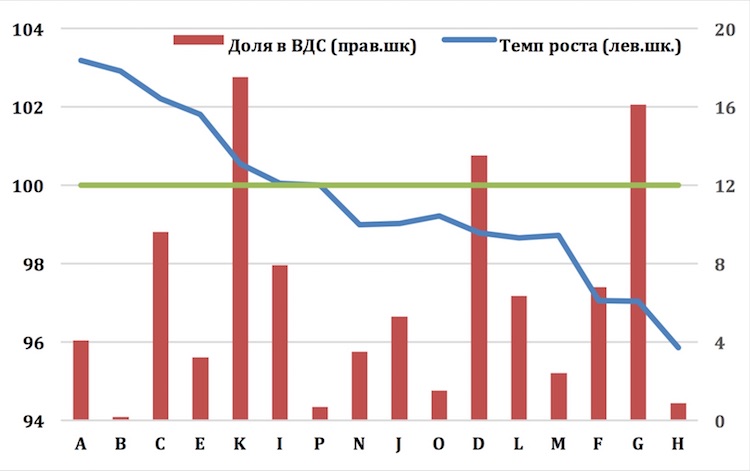

Chart 2. Russia’s GDP dynamics per industry (Q3, 2016 over Q3, 2015) and industries’ shares*

Source: Rosstat. (Red: gross value added; blue: growth rate).

Standstill Key Rate

The decision made by the Bank of Russia’s board of directors to keep the key rate unchanged should not surprise anyone. Even though most of the fears voiced by the Bank management in similar situations during the entire year (e.g. the threat of weaker fiscal policies) evaporated, the board of directors remained stubborn.

The Bank offered two key explanations: first, many factors that bring the inflation rate down are temporary; second, inflation expectations are slowly declining. It’s hard to argue against the first point; but as for the second point, I’m surprised that the Bank’s board of directors has ignored the assessments made by its own employees whose data shows a stable decline of inflation expectations following the falling inflation rate. At the same time, the board of directors is facing, tremblingly, these experts whose assessments clearly need to be corrected due to the “scale distortion:” the problem is that during the entire observation period, the inflation expectations have been noticeably higher than the inflation rate, which cannot be normal.

I often say that the Bank’s stubbornness when it comes to the key rate issue is unclear to me and its stance seems wrong. Perhaps the problem is not the Bank’s stubbornness or determination, but simply incompetence—when the position “if you don’t act, you won’t make a mistake” is perceived as the only right way.

Blind Vision

Estimates of the industrial output dynamic released by Rosstat in November 2016 looked unexpectedly high to many experts. This fact prompted speculation that Rosstat might have changed its methodology, which would be weird, since such changes are usually introduced at the beginning of the year. Rosstat didn’t blunder and issued an official statement that only complicated the matter further. First, it claims that no change has been made to the methodology. Which is great! Second, it says that regular adjustments to earlier estimates are standard statistical practice. It’s hard to counter this point and it should be viewed as normal. And third, Rosstat included a paragraph on the adjustment of the data collected in the first nine months of 2016 and on a “retrospective revision of the monthly production indices in 2015-2016, the results of which will be available in the first quarter of 2017.”

Translated into common parlance, it means that we should not trust the data on the industrial output dynamic released by Rosstat over the last two years, or the data that it will be publishing, until the “retrospective revision” is finished. In other words, Rosstat is depriving us (and, it seems, the government as well) of the latest information on Russia’s GDP dynamic.

The Turning Point?

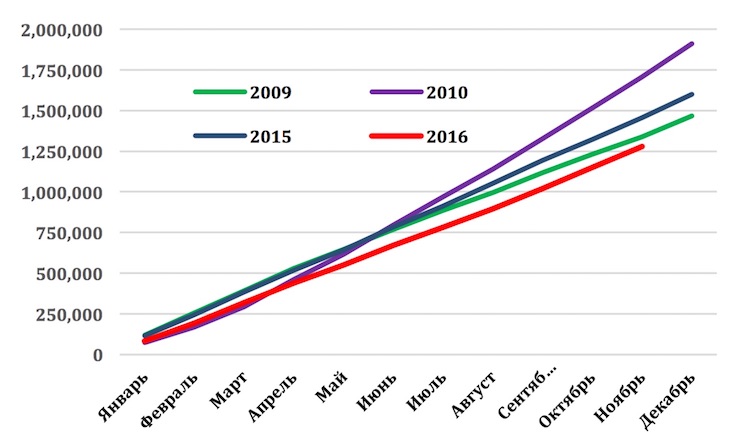

Here’s some news that may signify a turning point in Russian consumer sentiment: more automobiles were sold in November 2016 than in November 2015. Even if the gain is quite symbolic (0.6 percent, or 744 units), it puts an end to the nonstop decline in automobile sales over the past 43 months in a row, with only two exceptions—December 2013 and December 2014.

Obviously, this change does not secure a turning point just yet. Although it will be impossible for the Russian economy to reach the desired benchmark of a million and a half sold automobiles (still half the 2012 figure), and although it looks like we won’t even reach the 2009 level in sales, let us stay hopeful!

Chart 3: Sales of new automobiles in Russia, 2009-2016 (units, cumulative total from the beginning of the year; January through December)

Source: Association of European Business

Mortgage Is Stagnating

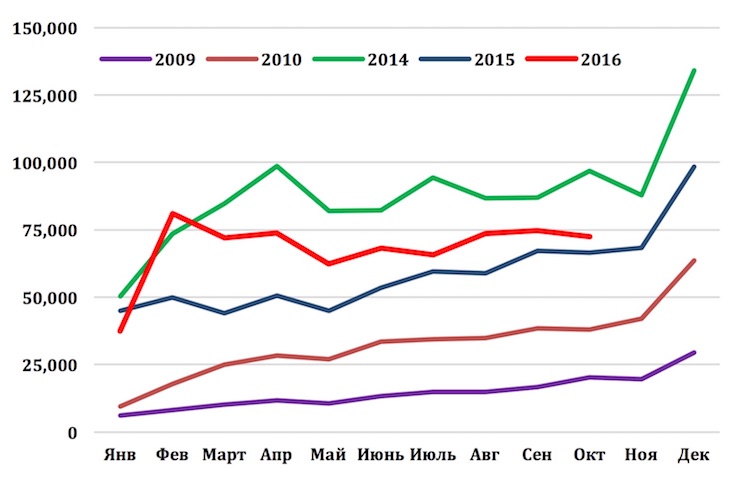

As opposed to automobile sales, recent data on mortgage lending do not look reassuring: the number of loans issued has been stagnating since last March, whereas in the post-crisis 2009-2010 and even in 2015 there was a consistent positive trend in the number of mortgage loans issued throughout a year. Today’s outlook is reminiscent of 2014, but that was the year of Crimea’s annexation, sanctions, oil-price drop...

Chart 4. Issuance of new mortgage credits in Russia, 2010–2016 (units, monthly; January through December)

Source: Bank of Russia

* Indicators: A – agriculture and forestry; B – fishery and fish-farming; C – extraction of minerals; D – manufacturing industry; E – generation and distribution of electrical energy, gas, and water; F – construction; G – wholesale and retail; H – hotels and restaurants; I – transport and communications; J – finance; K – real estate; L – government and defense, social security; M – education; N – healthcare and social services; O – other services; P – household activity.