In his latest commentary about recent developments in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, notes that Federal State Statistics Service new data creates more confusion about the state of the economy and argues that the Central Bank’s recent decision to keep the key rate unchanged may further damage the economy’s chances for growth.

Head of Russian Central Bank Elvira Nabiullina confirmed that the key rate remains at 10 percent per annum. Photo: Alexander Shcherbak / TASS

Rosstat surprises

Rosstat decided to gladden everyone by publishing revised Russian GDP data for 2014-2016. The fact of the revision itself is not strange at all, as this is typical practice for the work of statistics agencies. The problem in my view is that Rosstat’s new data contradicts both itself and the appraisals of other experts. For example, Rosstat confirms that a powerful driver of growth last year was non-petroleum exports, and data about the shipment of coal and metal ores shows an increase, respectively, of 16.4 and 13.7 percent compared with 2015. However, overall production in these sectors grew by 7 and 0.8 percent, respectively. Anything can happen in life, and often does, but it is difficult to believe that as of the end of last year Russian companies had amassed such huge reserves of unsold production. All the more so given that the statistics of reserves in the GDP structure indicate otherwise.

I'm not the only one surprised by the Rosstat data. It even reminds me of the Soviet joke about when the train carrying Brezhnev stopped and the General Secretary suggested rocking the car to give the illusion of motion. It seems to me that Rosstat is trying to create the illusion of growth, which is hard to believe in, and which cannot be confirmed thus far. At least, the trend in real wages doesn't suggest it is the case (not to mention the sorry state of consumption). Do you really believe that workers are ready to work and produce more without receiving adequate compensation for it?

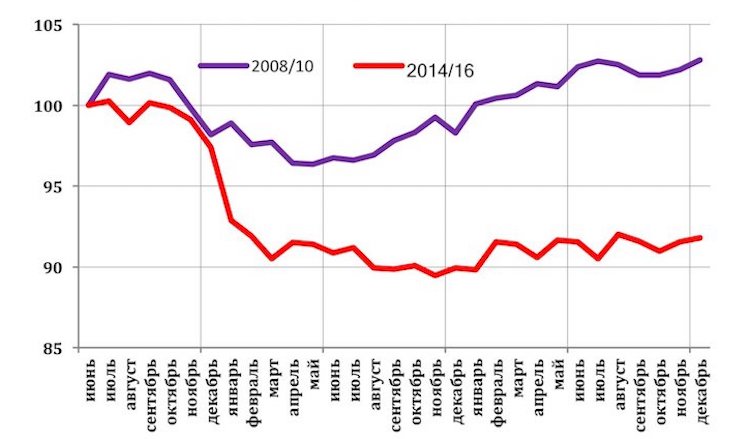

Chart 1. Construction trend, seasonally and calendar-adjusted, 2008-2010 and 2014-2016 (100 = June 2008 = June 2014)

Source: Rosstat; adjustment: Center for Development of the Higher School of Economics National Research University

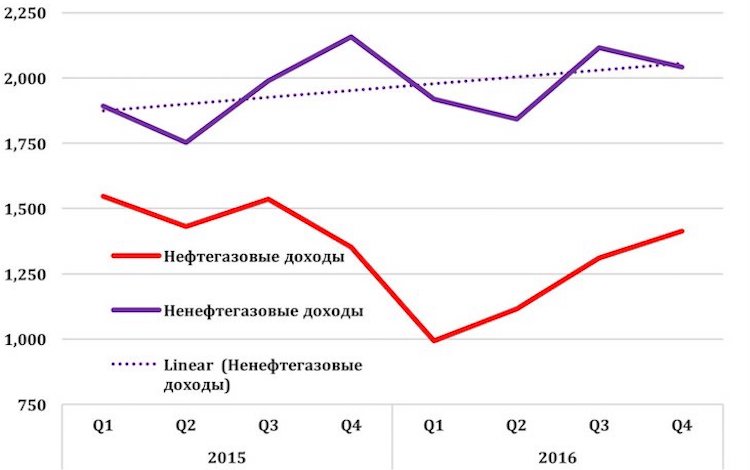

The Ministry of Finance Doesn't Feel Any Improvement

The federal budget income dynamics for 2015-2016 serve as evidence, if not of cunning on the part of Rosstat, then at least of a new methodology. As for petroleum income, everything looks logical and fully fits with other facts: the growth of oil prices in the first half of 2015 led to a growth of treasury income, the fall in oil prices by January of 2016 resulted in a fall in budget income, and then there was a new wave of growth in oil prices, which led to another growth in budget income.

Chart 2. Federal budget income, 2015-2016 (billion rubles per quarter).

Source: Ministry of Finance; red line: oil income; purple line: non-oil income.

As concerns non-petroleum income, the situation looks much less obvious: average growth amounts to a bit less than 1 percent per quarter, which, corrected for inflation, leaves no room for its growth in real terms. Moreover, it is obvious that in the fourth quarter, when according to Rosstat the economy began to pick up, nominal income growth disappeared altogether. Or rather, it turned out to be less than a year ago (naturally, from the total income of this quarter I subtracted income from the privatization of the bundle of shares of Rosneft, which are shown not as a source of financing of the deficit, but as dividends, i.e., as non-petroleum income).

The Central Bank Stands Its Ground

The Bank of Russia took the expected, but nonetheless no more rational, decision to keep the key interest rate at 10 percent. I wonder whether the Central Bank will one day manage to break the back of the economy.

I was also surprised by the conclusory sentence from the press release of the Central Bank concerning this decision: “Taking account of the changes in the foreign and domestic conditions, the chances of the Bank of Russia lowering the key rate in the first half of 2017 have lessened.” Don’t hold your breath! The following question immediately posed itself: what were the changed circumstances the Bank of Russia had in mind?

Here is what the press release has to say about it: “Annual inflation continues to lessen in accordance with the Bank of Russia's prediction . . . Inflation in the non-food market has substantially slowed.” To tell the truth, I don't see anything alarming in this.

Or this: “The restoration of economic activity in 2016 occurred somewhat more quickly than the Bank of Russia had expected.” Well, if our Central Bank is afraid of the “restoration of economic activity,” then don’t expect a lowering, but a raising of the rate, because economic recovery always follows a bottoming out.

But the crowning achievement of the authors of the press release was the following sentence: “Positive real interest rates will be supported at a level which will ensure demand for credit, without leading to a raising of the inflationary pressure, and will also preserve the stimulus to save.”

I wonder, do the authors even know that demand for credit in Russia is falling? That by the end of 2016 the volume of credit to the economy had dropped by 2.4 percent, taking account of the exchange rate difference? And if you remove the capitalization of interest from this indicator, and then add in 5.5 percent inflation, it turns out that in real terms the demand for credit has fallen by 9 to 10 percent! I wonder how much the demand for credit has to fall in order to finally be rid of inflationary risks?

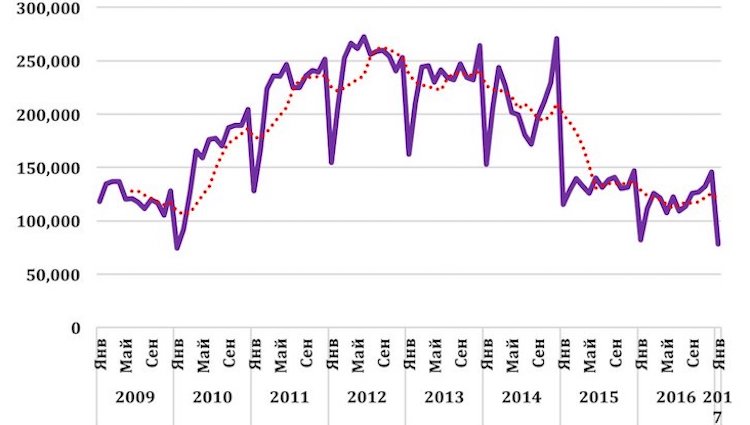

People Don't Need New Cars

The January data for sales of new passenger cars in Russia wrong-footed me. Analyzing the summary for the year, I pointed out that the situation had begun to improve noticeably by December, and hoped that in January this trend would strengthen with the new figures. But the fall in sales by 5 percent speaks to the fact that the public (at least those able to afford cars) doesn't believe that the economy hit the bottom.

It's clear that the January data per se doesn’t tell us very much: in the final analysis, January is not the best time to buy a car, as is readily seen in the chart. However, after the crisis of 2008 sales resumed in the fourth quarter of 2009, i.e. approximately one quarter after bottoming out. But this time? Incidentally, people have long since forgotten about getting past the bottom, and Rosstat can’t even say when this event occurred, so we just have to cool our heels.

Chart 3. Sales of new cars in Russia, 2009-2016 (units/month and sliding six-month average)

Source: Association of European Business

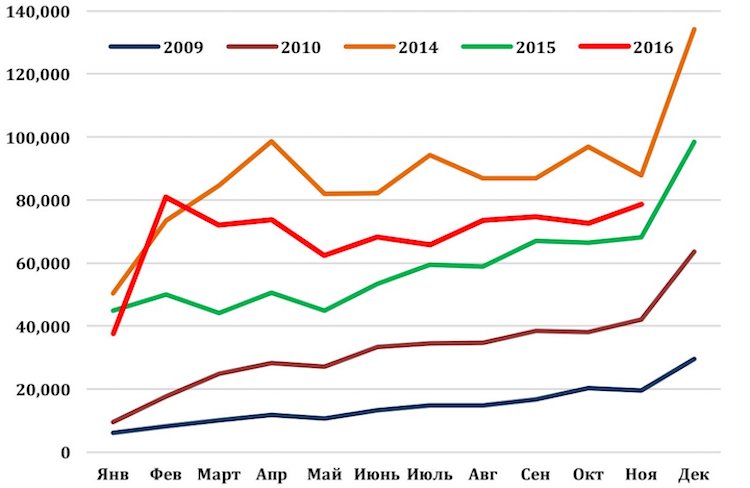

The Government Doesn’t Want a Revival

Data about the issuance of new mortgage credits comes out with about a two-month time lag, so today I will talk about the results of November, which (like the January sales of new cars) are not very representative—we will have to wait on the summaries of data for the year.

One thing is clear: the November data doesn’t add any optimism. All we can say is there’s a faint trend towards growth, or possibly stagnation. But, in combination with the Rosstat data about the accelerated fall in housing construction growth rates towards the end of the year, it alarms me. And these data cannot serve as an accurate explanation of the strange decision that the government took to end the support program for mortgage credit from budget funds.

I have said many times that this program is one of the most effective anti-crisis measures there is, because, on the one hand, it directly supports the end user (the population), and on the other, housing construction underpins a broad spectrum of sectors in the domestic economy. The argument in favor of abandoning this program was articulated by First Deputy Prime Minister Igor Shuvalov: “Commercial banks are already offering mortgage rates at 12 percent interest or lower. As part of the anti-crisis program we were in fact striving to reach a place where the borrower’s rate was no more than 12 percent.” This argument sounds absurd to me: when the decision to subsidize the rate at the expense of the budget was taken, the level of inflation was substantially higher than it is today. A 12-percent mortgage at 5-percent inflation? You have to be economically illiterate to borrow at such a rate.

Chart 4. Quantity of mortgage credits issued in Russia, 2010-2016 (units/month)

Source: Bank of Russia

The full version of this article has been published at openrussia.org (in Russian).