In his latest commentary about the recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, confirms that the fall in the Russian economy is over, but there is no growth to talk about.

Sergey Aleksashenko predicts strong volatility at the foreign exchange market in Russia. Photo: Anton Vaganov / TASS.

The Bank of Russia Has Grown Bolder

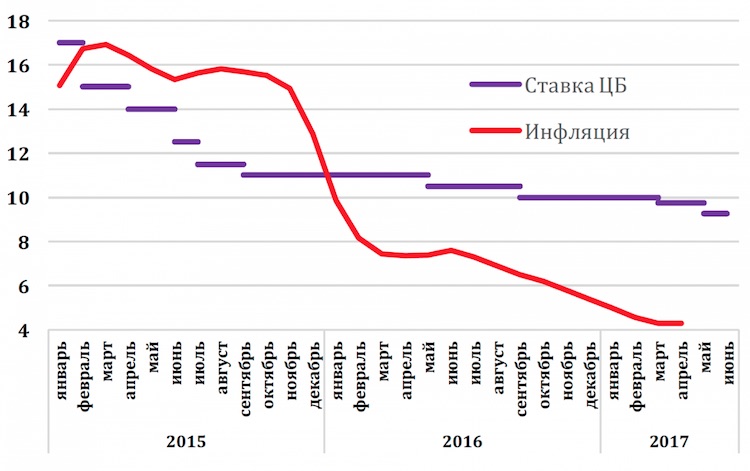

The Bank of Russia's decision to lower the key rate by 0.5 percent did not at all surprise me. Moreover, in my previous article I said that such a decision would appear fully logical even taking account of the super-cautious position of the Central Bank's leadership.

But the decision reached does not significantly soften the harshness of the monetary policy carried out by the Bank of Russia. The thing is, inflation in the Russian economy is falling more quickly than the key rate, and, therefore, the severity of the monetary policy being pursued (but not declared) has gradually increased. This phenomenon can be seen clearly in the chart shown below.

Chart 1. Trend in consumer inflation in Russia and key rate of the Bank of Russia (%)

Source: Rosstat, Bank of Russia. Red: inflation; purple: key rate.

This chart is plotted in “real time,” that is, the change in inflation and the key rate are shown on the same time scale. The Central Bank's rate works with a lag, which in Russian conditions is calculated at 6 to 9 months; if this is expressed on the chart, then it can be easily seen how strongly the Bank lags behind in taking the decision to lower rates, with each month strengthening the rigidity of its monetary policy.

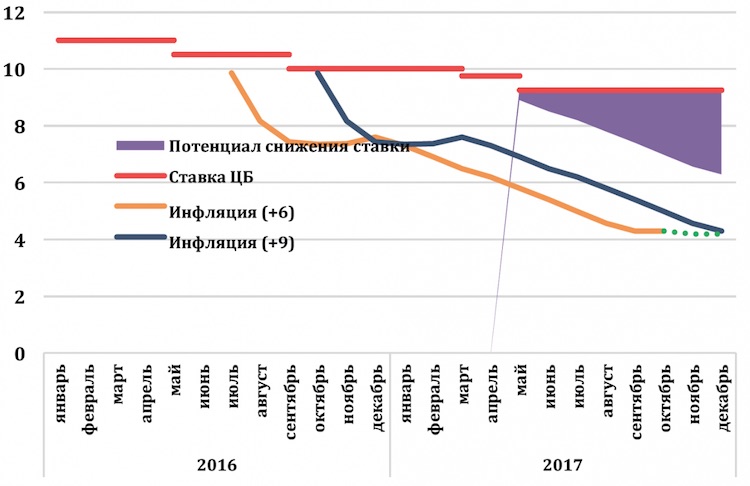

Assuming that inflation, in accordance with the prediction of the Bank of Russia, will fall by the end of the year and that over the medium term will be around 4 percent per year (which in my view is excessively high), then the normal rate of the Bank of Russia could be at the level of 6 percent, and, consequently, the potential lowering of the key rate right now is 325 basis points. I am far from thinking that the Bank of Russia will lower it that much in one or two meetings, but if it “prolongs the pleasure” as it has before, then the Russian economy will feel the pinch.

Chart 2. Trend in consumer inflation in Russia

Source: Rosstat, Bank of Russia. Purple: potential for the key rate decrease; red: key rate; orange, blue: inflation.

Why the Ruble Is Strengthening

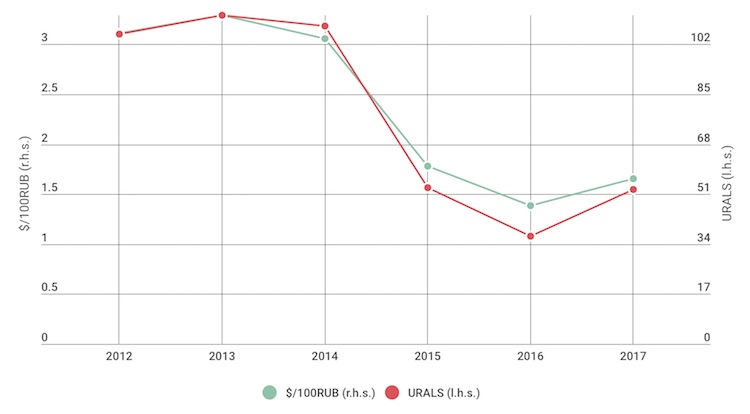

These days I’m often asked: why is the ruble strengthening? And when will it crash? I have to disappoint you: the fact that the exchange rate of the ruble mirrors the change in the oil price with surprising precision has long been the norm. In this sense there is nothing surprising taking place in the currency market. That can be seen clearly in the chart below. If the current level of oil prices holds, then no sharp changes should be expected in the next few months.

According to the Center for Development, a steady trend of rapid growth in imports is emerging. If it keeps up, by the end of the summer the ruble exchange rate may come under strong pressure. The fact is that the growth in foreign currency earnings as a result of the recovery of oil prices has already fully been reflected in the balance of payments and this process has occurred very abruptly. Unlike the sudden spike in export earnings, the recovery of the demand for imports is monotonous, but very steady. Judging by the customs statistics, growth in imports can be seen in all the commodity groups, which is not surprising given the rapid strengthening of the exchange rate of the ruble over the last year. For this reason, it is highly likely that import growth will develop a steady trend.

If we add to this the seasonal growth in importer demand for foreign currency, which is traditional for the end of summer, and the inevitable outflow of ruble assets from non-residents in accordance with the lowering of the key rate by the Bank of Russia, then I am ready to suppose that serious volatility awaits us on the foreign currency market.

Chart 3. Trend in price for oil of URALS brand ($/barrel) and exchange rate of the Russian ruble ($/100 rubles), 2012-2017.

Source: Bloomberg, Bank of Russia

A Five-Year Plan for Slow Growth?

Looking at the trend in the Russian Development Bank (VEB) Index, which is put together by bank experts on the basis of monthly estimates of GDP, we can reach several conclusions.

Chart 4. VEB Index – latest estimate of GDP with seasonality and the calendar factor removed (100 = January 1999)

Source: VEB

Firstly, the economic downturn is over, suggesting a weak growth trend.

Secondly, by GDP volume the Russian economy is on a level with the mid-2008, i.e. the Kremlin's economic policy over the last eight years has produced no growth whatsoever.

Thirdly, the speed of recovery of the Russian economy, which VEB says began late summer last year, is so insignificant (less than 0.5 percent for eight months), that in order to reach the peak level of July 2014, the Russian economy will need more than five years.

Rosstat and GDP

Although practically all the experts speak about the recovery of growth in the Russian economy, I don't see the process as steady.

First, we should not forget that Rosstat seriously revised the historical series, thereby improving the GDP dynamics for industry and manufacturing over the last two years. At the same time, Rosstat remains unable to publish data about GDP dynamics according to the standard method used in the world–quarter over quarter on an annualized basis (the data for the Russian economy end with 2011).

An upward adjustment of the GDP data was carried out based on a revaluation of small business, which, in the statisticians' opinion, for some reason has seen rapid growth in the last two years, carrying the whole economy with it. The improvement in the data for industry was the result of revising the set of commodity groups, where the weighting of the defense complex was clearly increased. However, the rate of growth of the military-industrial sector is steadily falling from year to year: by 15 percent in 2013; 12 percent in 2015; and 10 percent in 2016. Taking account of the reduction in financing of military expenditures in 2017, we can expect at least a continuation of this trend, and perhaps an actual halt in growth.

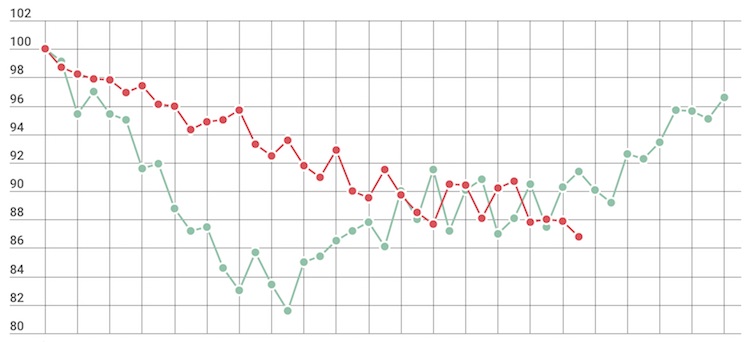

Chart 5. Trend in construction, seasonally and calendar-adjusted, 2008-2011 and 2014-2017 (100 = June 2008 = June 2014)

Source: Rosstat, smoothing by the Center for Development of the Higher School of Economics National Research University

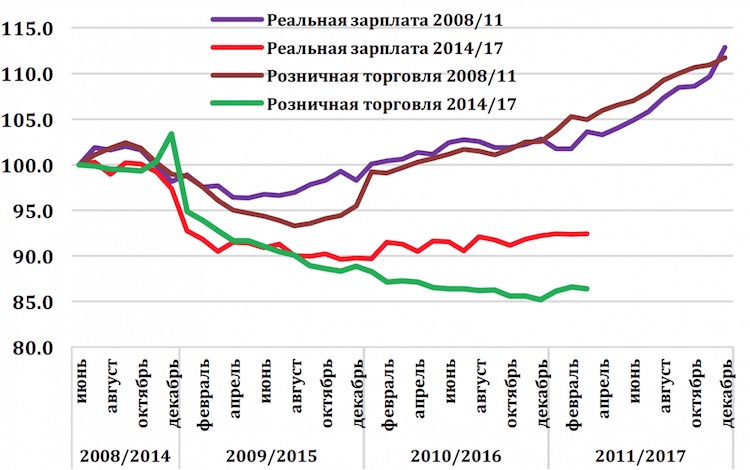

Secondly, the data for the first quarter do not look at all good: the minimal growth in industry (0.1 percent); the growth of cargo turnover with Russian Railways posting a loss (the growth in cargo was achieved thanks to coal, the transportation of which is unprofitable for the railroad); the sharp decline in construction, especially in housing; the halt of growth in real wages accompanied by falling inflation; and the growth of retail sales achieved solely thanks to one-time pension supplements.

I don't doubt that Rosstat will report growth in the economy in the first quarter, but cannot for the life of me understand why in a non-growing economy enterprises will increase their reserves for a second year in a row (this is precisely how Rosstat explains the Russian economy’s transition to growth at the end of last year).

Chart 6. Trend in real wages and retail turnover, 2008-2011 and 2014-2017 (100 = June 2008 = June 2014)

Source: Rosstat, smoothing by the Center for Development of the Higher School of Economics National Research University. Purple, red: real wages; brown, green: retail turnover.

Minus 2 percent

There is a great report entitled “The Russian Labor Market: Trends, Institutions, and Structural Changes,” prepared at the request of the Center for Strategic Studies by the Higher School of Economics. The report is long (more than 180 pages), and packed with figures and analysis. It's not light reading, but interesting.

The part of the report that merits special attention concerns the next 15 years, during which there will be very serious changes in the Russian economy concerning the quantity and quality of the labor force. The report's authors talk about a forthcoming reduction during that period in the size of the workforce in Russia by 6.6 million persons, in other words, by more than 8.5 percent. This means that the size of the workforce is set to fall annually by 1.08 percent, and all other conditions being equal, this will cause an economic slowdown of almost 0.9 percent annually.

For comparison it is worth noting that in the period of 2000-2008, when the Russian economy grew at an average rate of 7 percent per year, the number of those employed in the economy (again owing to demographic factors) grew by 6 million persons (or by 9%), i.e. by one percent annually, which gave the economy an additional one percent growth. So, the demographic factor substantially changes the economic dynamics in Russia: the difference between +1 percent in 2000-2008 and minus 0.9 percent in 2016-2030 comprises almost two percent of annual growth.

This English translation of this article was edited and abridged for clarity.