Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution and former deputy chairman of the Russian Central Bank, comments on recent key developments impacting the Russian economy.

Businessman Dmitri Kamenshchik, owner of the Domodedovo airport in Moscow, was arrested on February 9, 2016. Photo: Artyom Geodakyan / TASS

The Arrest of Dmitry Kamenshchik

The arrest of Dmitry Kamenshchik, owner of Domodedovo Airport in Moscow, was the most important development in the Russian economy last week. There can be no doubt authorities arrested him in order to seize his property. In other words, we’ve witnessed a reincarnation of the Yukos case. If there was one thing Russian authorities could have done to ultimately ruin any hope of the country’s economy returning to growth, this was surely it: a public demonstration that property in Russia (be it a Moscow kiosk or assets worth billions of rubles) is not protected at all.

I’ve said it many times before and will repeat again here: the major reason for the current crisis in the Russian economy is businesses’ unwillingness to invest in development. Just think: who would invest in a project with a return on investment of five to seven years or more, after seeing how businessmen are put behind bars?

No “Standstill”

It’s difficult to provide an accurate analysis of Russia’s economic performance in January, as at least third of the month can be accounted for by the holidays (New Year holidays in Russia typically last through January 11). Plus, the seasonal factor has a high impact on the infrastructure industry. Still, some economists have assessed the current situation as “stagnation,” while Russia’s economy minister Aleksei Ulyukayev has described it as a “surplace,” or “standstill.”

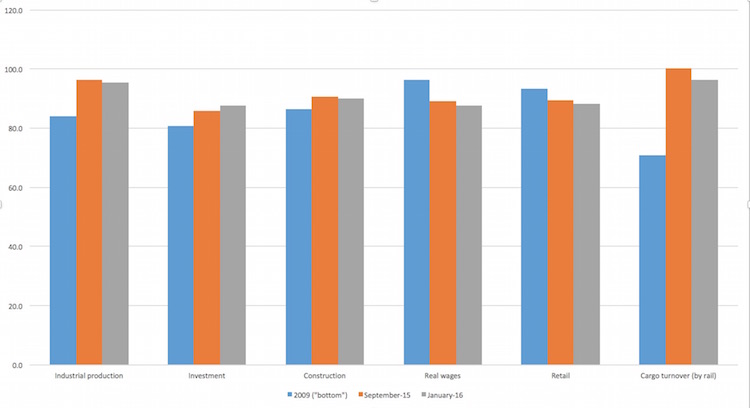

Chart 1. Dynamics of the Russian Economy by Several Indices (100 = June 2008 or 2014)

Source: Rosstat; seasonal and calendar adjustment by HSE Development Center

To understand whether the Russian economy is actually “standing still” (something economists can only dream of), I decided to compare the economy’s current state to the parameters of the third quarter in 2015, adjusting for seasonal and calendar factors. (By the way, back in the fall, Ulyukayev claimed that the economy had started to grow.) Such a comparison makes sense, as the seasonal volatility of many indices cannot be adequately adjusted for if compared month-to-month.

Some readers are not going to like my conclusion, but I can’t put it any other way: the Russian economy continues to slowly slide downhill. Almost all the indices are deteriorating, except for investment (which will doubtless catch up with the general trend later this year). The economy appears unable to stabilize or “stand still.”

Meanwhile, the Russian finance ministry has revealed its long-term outlook—up to 2030—in which it predicts that if oil prices remain at $40 per barrel (in real terms, accounting for an annual increase of $1 per barrel), the economy can only grow by 1 to 1.5 percent a year. Any hopes for a higher growth rate—2 to 3 percent a year—are directly linked to higher oil prices and structural changes in the economy that would yield higher capital returns and productivity growth. As usual, the authors of the forecast do not clarify how the latter changes might be brought about.

The Oil Deal

The agreement between Russia, Saudi Arabia, Qatar, and Venezuela to freeze oil production levels will not change the price dynamics in upcoming months. For one thing, restrictions were applied based on January 2016 production levels, when they were at their maximum. If all these countries adhere to the agreement, at the end of the year daily output will have increased by 500 to 700 thousand barrels—thus compensating for the probable decrease of U.S. oil production. For another, Iraq and Iran—two countries with great potential and aspiration for higher oil production—did not join the agreement for obvious reasons.

For Russia, the mere fact that this agreement took place signals that authorities are seriously concerned about budget issues and are fully aware that a further drop in oil prices will force them to make a difficult choice: between raising inflation and making additional budgetary cuts. This unappealing prospect has pushed Russia to make the restrictive cartel agreement—something the government has been refusing to do for years.

Banking System No Better Than the Economy

January operational statistics on the performance of the banking system offer no good news. Though last month’s results turned out to be better than those of 2015 (profits leveled at 32 billion rubles, or $420.9 million, while losses were at 24 billion rubles, or $315.7 million), this is hardly cause for euphoria. Last year banks put 282 billion rubles ($3.71 billion) into reserves; this year that figure was only 98 billion ($1.29 billion). Thus, this year their financial result before reserves turned out to be lower than last year’s by 60 percent—130 billion rubles vs. 312 billion ($1.71 billion vs. $4.1 billion).

Another piece of bad news is that post-due debts owed by private individuals continued to grow, while borrowing demand dropped—a telling sign that the emerging consumption recovery that some observers announced earlier has not taken place. In a bit of scarce good news, the corporate sector’s borrowing demand continued to grow (hopefully this growth does not reflect restructuring of “bad” debt).

Bank of Russia Outlook

Bank of Russia recently released its January outlook on trending inflation, which, as expected, has gone down along with the annual 12-month rate, though the former remained 1 percent higher than the latter. The bank’s experts highlighted that fact, claiming that this dynamic “confirms the increasing risk that the inflation rate might deviate from the annual target by the end of 2017” (i.e., will be higher by 4 percent). I agree with this assessment, but I’m afraid I have to make an even more pessimistic projection: the inflation rate will unpleasantly surprise us as early as this year.

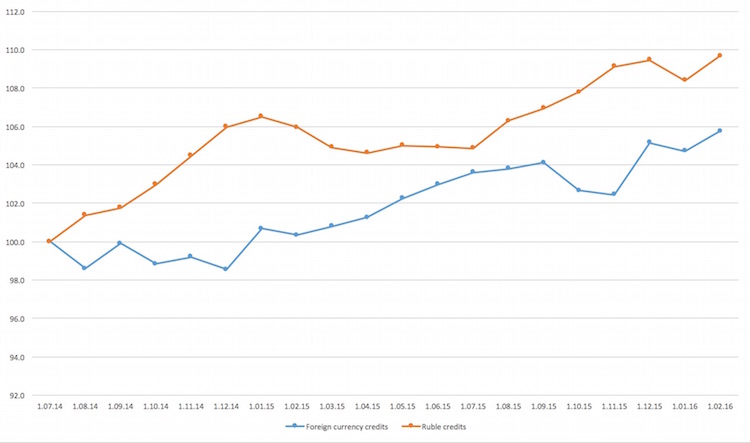

Meanwhile, Bank of Russia head Elvira Nabiullina made a tough announcement regarding the campaign forcing banks to lower their dollar balances. I understand the bank’s management: the share of foreign currency deposits owned by firms is 50 percent, while the share held by private individuals is 30 percent. This ratio in favor of firms may seem unpatriotic from an official angle, given Russia’s uneasy international situation. But I doubt the policy instruments suggested by the bank—increasing the level of required reserves and pushing for lower interest rates—will be successful. I wonder: does the bank really think people and firms keep their savings in foreign currencies only because interest rates are high (while, in fact, they are rarely higher than 2.5 percent)? Does it really think that saving in rubles at an 8-percent interest rate is profitable, when the current inflation rate is 10 percent and the ruble has devalued more than twofold over the last two years?

I was even more surprised when I looked at the statistical data published by the Bank of Russia itself. How did the conversation about “dollarization of the banking business” even come about? As it turns out, the very increase in the share of foreign currency credits and deposits that the bank is so worried about has been entirely caused by the devaluation of the ruble. In the charts below, you can see that foreign currency deposits held by both private individuals and the corporate sector (in dollar terms) have not grown, but, in fact, have slightly decreased since July 1, 2014 (the latest date before financial sanctions against Russia were imposed by the West, and the latest date at which oil prices were over $100 per barrel). At the same time, ruble deposits have visibly grown.

Chart 2. Dynamics of the Volume of Deposits Held by Private Individuals and Legal Entities in Russian Banks (July 1, 2014 = 100)

Source: Bank of Russia

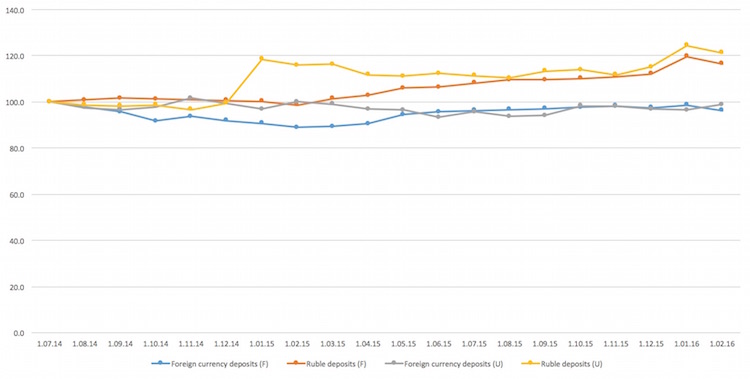

As for the banks’ active balances, similar trends can be observed: corporate debt in ruble terms is growing twice as fast as it is in foreign currency terms. And one can forget about private debt in foreign currency terms, as it accounts for less than 2.5 percent of total bank debt and, since July 2014, has decreased by 40 percent in dollar terms.

Chart 3: Dynamics of Loans Credited by Russian Banks (July 1, 2014 = 100)

Source: Bank of Russia

If all the decisions made by Bank of Russia’s oversight department are based on similar data, this explains why its banks are collapsing one by one, forcing the government to fulfill all of its financial obligations. In reality, the banking system’s structure of assets and liabilities in foreign currency terms reflects the structure of the Russian economy, which can be split into two parts: exporters, who receive profits and loans in foreign currency; and the rest, who operate in rubles. It would be naïve to assume that any regulations imposed by Bank of Russia could change this situation.

5-Percent Military Cuts

Finally, the sudden news that the Russian government will be cutting its military expenses by 5 percent this year allows one to make two conclusions: First, president Putin has acknowledged that the country’s budget is in critical condition. It’s impossible to cut military expenses without his personal approval, and I’d like to remind readers that the government made provisions for even larger cuts (300 billion rubles) in its finalized draft of the 2016 budget before it was sent to the State Duma for reading. Back then, the president rejected the cuts, and military spending remained in full. One can assume that the finance ministry has now presented a more convincing set of arguments (a sharp decrease in income level, significant leftover funds from last year’s budget) to make Putin change his mind and greenlight the cuts.

Second, the cuts were made to arms procurement, while current expenses of the defense ministry are not subject to any cuts. This will inevitably lead to a slowdown in the defense industry, which has of late been the only industry showing positive dynamics (save for exportable raw material industries). The 850 billion rubles in military expenses that were not utilized by the 2015 budget should have impacted the way Rosstat assessed its data in terms of GDP. This money amounts to 1 percent of GDP, and it is just sitting in the accounts of the banking system. Even if the statistic service doesn’t change its outlook, it seems that in 2016, Russia’s industrial sector will continue to decline.

This article originally appeared in Russian at openrussia.org.