In his latest commentary on recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes the outlines of Russian budgetary policy and pension reform, the latest data about the automotive and mortgage markets, the possible sale by Mikhail Prokhorov of his business, and Gazprom’s dubious plans. His conclusion: it is becoming less and less comfortable to live and do business in Russia, even for those who are loyal to the system.

Rumors that Mikhail Prokhorov (depicted above) is considering the sale of all parts of his Russian business constitute an obvious symptom of the unfavorable institutional environment in Russia. Photo: Artyom Korotayev / TASS

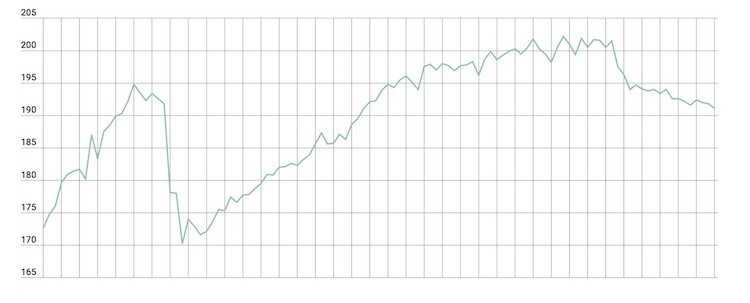

The GDP Dynamic Is Too Stable

The VEB (Russian Development Bank) Index—the monthly estimate of Russian GDP—dropped sharply in May as expected. As a result, over the last 12 months GDP fell by a bit less than 1.5 percent, which is clearly not a catastrophe, but speaks to the continuing monotonous downhill slide of the economy.

Chart 1. The VEB Index–monthly assessment of GDP, not seasonally- or calendar-adjusted (100 = January 1999)

Source: VEB

How Can the Economy Be Driven into Stagnation?

The outlines of a budget policy for the next few years are little by little beginning to take shape in decisions at the governmental level. The Finance Ministry’s idea—a deficit of 3 percent of GDP in 2017 and a reduction for its sake in any expenditures—is not encountering any serious resistance. In all likelihood, it has already been approved at the highest level, and that is well understood by everyone.

Because the budget forecast does not include growth of the economy or of oil prices, an increase in incomes cannot be observed in the budget plan. Consequently, the key questions that will have people crossing swords over the next few weeks are these: 1) How much will the indexation of wages of government employees and of pensions be next year (if it occurs at all)? 2) Will military expenditures be reduced or not in comparison to the level announced a year ago? The amount by which all remaining budgetary expenditures will be reduced will be clear only after these questions are answered. But it obviously will be no less than 10 percent in real terms (accounting for 6 percent inflation).

I have already spoken repeatedly about this and I’ll say it again: such a budgetary policy maintains stagnation in the Russian economy, making it all the more difficult to emerge from it the longer it continues.

The New Is the Not-Yet-Forgotten Old

The Finance Ministry and the Bank of Russia announced that they are ready to offer a joint proposal on pension reform, which, alas, will not be novel either in its contents or in its principles.

Remember, we are talking about the fifth restructuring of the pension system during the rule of president Vladimir Putin, and each time the authorities have promised it was the last. As before, the only goal of the proposals is the lessening of the pension system’s pressure on the federal budget over the next two to three years. The means are also the customary ones—raising taxes, which this time is termed “cancellation of the mandatory contributory system.” And again there is an absence of any clarity whatsoever concerning what awaits the pension system in 10, 15, or 20 years.

You know, given such premises, I’m ready to bet that in three or four years (and maybe sooner) we will have yet another pension reform.

In addition, as part of the discussion about the 2017 budget, representatives of the Labor Ministry announced that the contributory part of pensions will again be confiscated, and that this isn’t subject to discussion.

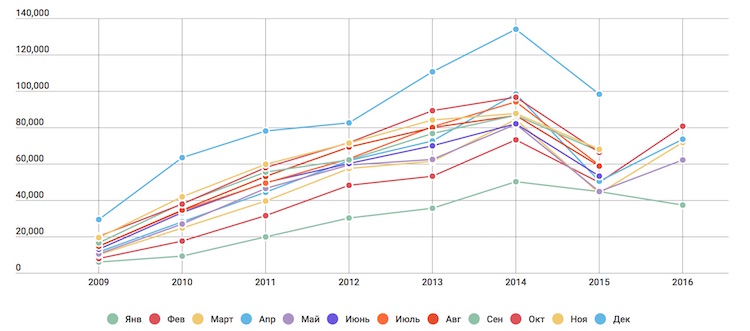

Mortgage Market: Cheerless as Expected

The sharp decrease in the number of mortgage credits issued in May seemed, on the one hand, predictable: there were many holidays that month. On the other hand, it is clear that the boom we witnessed in the beginning of the year is gradually dying down.

Chart 2. Number of Mortgage Credits Issued in Russia, monthly (units)

Source: Bank of Russia (January through December).

Optimists will stress that this year the number of credits issued is almost 40 percent greater than last year. Pessimists, while acknowledging this, will stress that by comparison with 2014, the number of credits issued is down by 16 percent.

I continue to believe that the results for June will in large measure be indicative and will provide a basis for a forecast through the end of the year.

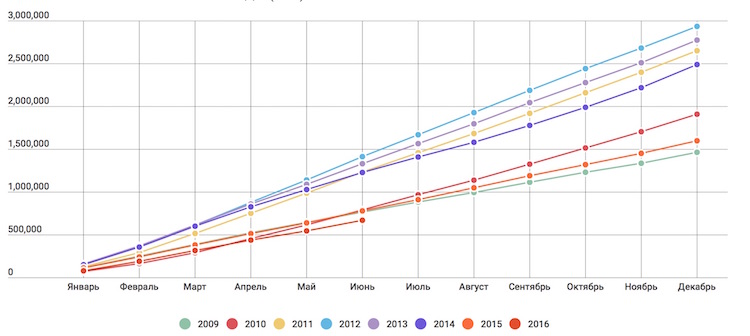

Automotive Market: From Bad to Worse

In the automotive market, the situation continues to worsen—the sale of new automobiles in June again fell (down by 12.5 percent compared to June of last year). The end results of the half-year look still gloomier: -14 percent growth for 2016.

So far there is no reason to expect a break in this trend, and this forced the Association of European Business to substantially worsen its forecast—to 1.44 million automobiles by the end of the year, with the proviso that even this forecast may be too optimistic, as it envisages a twofold slowing in the falloff of sales in the second half of the year.

Chart 3. Sales of New Passenger Cars in Russia, year-to-date (units)

Source: Association of European Business (January through December).

Where There’s Smoke, There’s Fire

Rumors that Mikhail Prokhorov has either made a decision about, or is ready to consider proposals for the sale of all parts of his Russian business constitute an obvious symptom of the unfavorable institutional environment in Russia. Having successfully sold his share of Norilsk Nickel on the eve of the 2008 crisis, Prokhorov tried to find a use for his capital in Russia for several years—in the companies Polius Gold, Kvadra, Uralkalii, his media holding, the Renaissance financial group, and the MFK Bank—but none of these (for various reasons) “took off.”

Concurrently with the above, Prokhorov made several attempts to move into the public political arena, positioning himself as a technocrat loyal to the authorities; but in this he also failed to achieve success, because he tried to be an autonomous and independent player, which in the Kremlin’s view is not acceptable in Russian politics.

I don’t know what plans may really be brewing in the oligarch’s head, but I understand very well that it’s practically impossible to find a use for his billions in Russia—the economy simply doesn’t generate new projects on such a scale, and Prokhorov isn’t interested in buying old businesses. That said, Prokhorov’s experience shows that the only stable model for oligarchical business that has a chance of surviving in Russia is the cash cow: management of an asset that constantly generates a cash flow that can be “piled up” in some safe harbor somewhere.

Whichever option Prokhorov chooses—whether he “takes retirement,” or, like Mikhail Fridman, moves the center of his business activity abroad—won’t be good for the investment climate in Russia. If even a businessman so loyal to the authorities finds doing business uncomfortable in Russia, what does that say about the others?

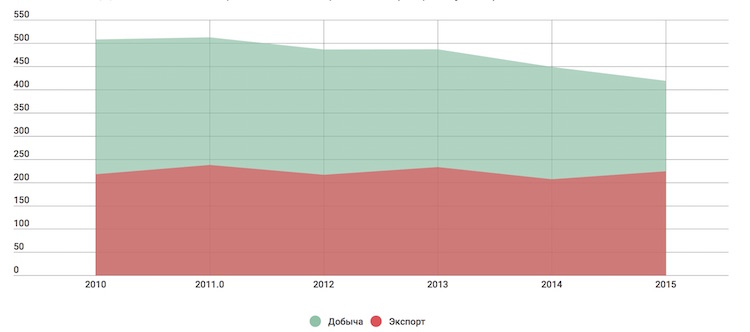

Gazprom’s “Excellent” Strategy

Strategy is not just a bunch of words, goals, and presentations; often actions and facts tell a lot more about it. And this is especially true of the Russian “national patrimony,” Gazprom.

The chart below shows that over the last five years, the gas monopoly lowered its gas production by almost 20 percent (an optimistic forecast for this year is zero growth; a pessimistic one is -7 to -8 percent), and at the same time the aggregate volume of exports (to all countries) remains nearly stable. In other words, all of this falloff reflects a loss on the domestic market. And now add to that the fact that for the last eight years, the company has invested approximately $40 billion per year, from which more than half went to the development of the gas transportation system, and another 20 percent to increasing the capacity of gas extraction. The result is that the capacity for gas extraction today exceeds by 50 percent the amount produced; the capacity of the existing export gas pipelines to non-CIS countries exceeds by 60 percent the volume exported; and the capacity of the pipelines that are planned and under construction is equal to current exports to non-CIS countries.

Chart 4. Extraction and Export of Gas by Gazprom (billions of cubic meters)

Source: Gazprom (Green: extraction; red: export).

If I didn’t know Russian reality, I might say that Gazprom is getting ready to repeat the Saudi strategy—a share of the market at any price—in Europe. Indeed, production can be increased sufficiently quickly, and the gas pipelines are in place and idle; just lower the price and conquer the market! But . . . such a theory has little relationship to reality. At least, no tactical actions of Gazprom on the European market (including Ukraine) confirm it.

Still, what has happened with Gazprom during the last eight years perfectly proves the well-known rule: your (Gazprom’s) expenditures are always someone else’s income! If we remember that the monopoly builders of the gas pipelines in Russia are friends of President Putin, and, being a bit bold, we suppose that they earn only 10 percent on these projects, it appears that since 2008 a pair of Russian businessmen have earned $16 billion. So who then can say that Gazprom’s strategy is a bad one?

An Elegant Solution

After two decades of unsuccessful efforts to force banks to grow their capital, the Russian Central Bank has found an elegant solution to this problem: if the necessary measures are taken, half a year from now Russian banks will be divided into “regional” and “inter-regional” ones. For the first category, the required capital will remain the same, at the level established by law—300 million rubles—and for the second category, it will be raised to one billion rubles.

On the one hand, by today’s price standards, one billion rubles for a bank is not all that much; but on the other hand, inasmuch as these changes will be introduced by decisions of the Bank of Russia (and not by a law), we can expect that the Bank of Russia will not stop there.