In his latest commentary about recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes yet another decision of the Central Bank not to raise the key rate, the trend in issuance of mortgage credits, and the diminishing reserves of the Russian budget.

During his working visit to Crimea this May, Russia's prime minister Dmitry Medvedev tried to show his support for the region's pensioners as much as he could. His phrase about how the budget is short of money became proverbial. Photo: Dmitry Astakhov / TASS

A Vague Decision

The decision of Bank of Russia’s board of directors not to lower the key rate, leaving it at the level of 10.5 percent per annum, is not surprising: essentially, nothing new has happened in the economy, and the Central Bank didn’t promise to lower the rate. Nonetheless, the decision and the arguments behind it are important. They are as follows:

1) Inflation is decreasing as predicted. Although the base rate of inflation and inflation expectations have slowed the decline, a further decrease in inflation is inevitable due to demand limitations, heavy crops, and a slowdown in the indexation of utility rates.

2) A revival of production activity (the reasons for which remain unclear) is occurring against a backdrop of weak demand and will not lead to an increase in consumer prices.

3) There is still uncertainty about budgetary consolidation and specifically the indexation of budgetary salaries and pensions. The emerging trend of increasing wages and decreasing deposit rates can result in less motivation for households to save.

Obviously, the first two arguments work in favor of lowering the rate. It should be emphasized that both describe a real situation, in other words, what is happening in the economy—a steady lowering of inflation. The third argument sounds downright ridiculous to me: there is always uncertainty in the economy, especially in the Russian economy, where one person who is not restrained by anything or anybody can make any decision at any time.

If we speak of Bank of Russia’s fears concerning a reduced tendency to save if wages rise and interest rates are lowered, in my view, we must not forget that only one third of Russians have any savings, and two thirds live paycheck to paycheck. Moreover, the majority of savings are held by large depositors who, firstly, understand very well that savings are necessary, and secondly, if they do decide to consume more and save less, will buy higher quality and most likely imported goods, which don’t figure into Rosstat’s basket of consumer goods.

Thus, the Bank of Russia’s decision is weakly reasoned, leading me to this conclusion: either the Central Bank has other reasons that for some reason weren’t made public, or it simply doesn’t understand that lowering the rate by 350 basis points in the real rate (and add in 200–300 points of bank margin) for an economy that is in recession is like lowering the oxygen level in an intensive care ward.

The Sentiment Is No Better

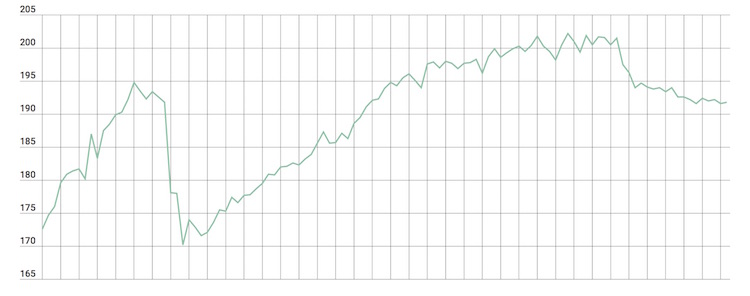

The Economic Ministry and the Russian Development Bank (VEB) have published their assessments of the trend in GDP, which don’t differ much from one another. The Economic Ministry speaks about stagnation in June, and the VEB about weak growth (0.1 percent). This difference isn’t significant, because any quick assessment of the GDP trend must be made under conditions of incomplete information. What is important is that for five quarters now we have seen an oscillation of the monthly indicators around the zero mark with a weak negative trend at a level of -1 percent on a year-on-year basis, and a cumulative decline as compared to the end of 2014 nearing 5 percent.

What really surprised me was the statement of Economic Minister Alexey Ulyukaev , who moderated his optimism by saying he expects zero variation in the third quarter, although not long ago he spoke confidently about the impending start of growth.

Chart 1. The VEB index – latest assessment of GDP with seasonal and calendar factors removed (100 = January 1999)

Source: VEB

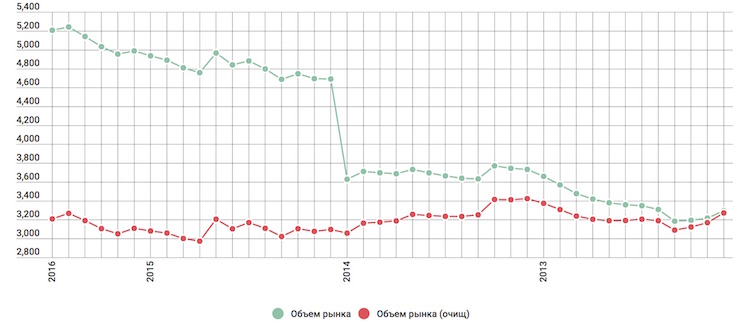

Mortgage Credits: Premature Joy?

“The growth of mortgage housing credit in Russia continues!” the Central Bank has joyously informed us. And, on the one hand, that’s true. Even though after the boom in credit activity at the beginning of the year—when borrowers feared the cancellation of the government program of subsidizing interest rates—the number of credits issued slacked off, the indicators for this year are still second only to the record of 2014. On the other hand . . . acorns were good until bread was discovered.

When you take out a long-term mortgage, at some point the current interest rates on credit may be lower than those you agreed to at the outset. And then, of course, you begin to wonder whether it’s possible to replace your old line of credit with a new one, at a lower rate. Many banks like such refinancing and gladly accommodate their clients. But from the analyst’s point of view, a distinction should be made between new credits and older refinanced credits.

The Bank of Russia statistics don’t provide such information, but you can get it if you do a few simple calculations. True, this gives you not the number of credits, but rather their total amount, but for the purposes of evaluating the trend you can ignore that fact.

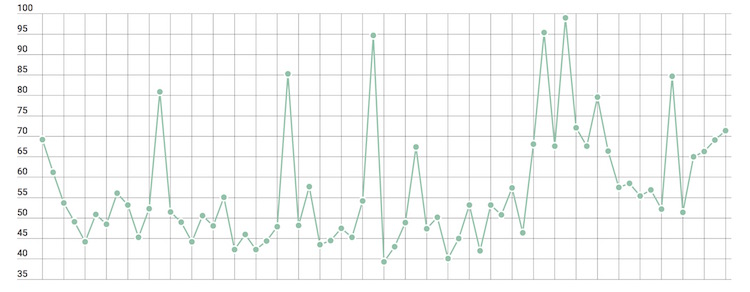

Chart 2. Number of mortgage credits issued in Russia, year-to-date (units)

Source: Bank of Russia (from January to December)

Chart 3 clearly shows that since the beginning of 2015, when the program of subsidizing mortgage interest rates began, the share of credits issued for refinancing has sharply increased, growing from a range of 40–60 percent to a range of 60–80 percent. Moreover, in the first half of this year, an obvious growing trend in this indicator can be observed.

The conclusion is simple: the issuance of mortgage credits in Russia is continuing to grow, but the volume of new credits is growing much more slowly, on a clearly declining trajectory.

Chart 3. Share of mortgage credits issued in Russia, intended for debt refinancing, and the six-month moving average

Source: Bank of Russia

Although it seems strange to me, it’s possible that this explains the decisive promotional statement president Vladimir Putin made in his meeting with Sberbank chairman Herman Gref when he proclaimed it necessary that “your (Sberbank’s) clients not think that it’s better to wait and not take out mortgages,” because “it’s better to do it now.” But it seems the president’s reasoning was spontaneous—“Because inflationary developments are taking place”—and worked against the Central Bank and its efforts to dampen inflation, rather than in favor of accelerating the receipt of mortgage credits.

Whether this is so and whether the public is ready to believe Putin’s economic forecasts will be clear from the economic results of July and August.

Help from Non-Residents

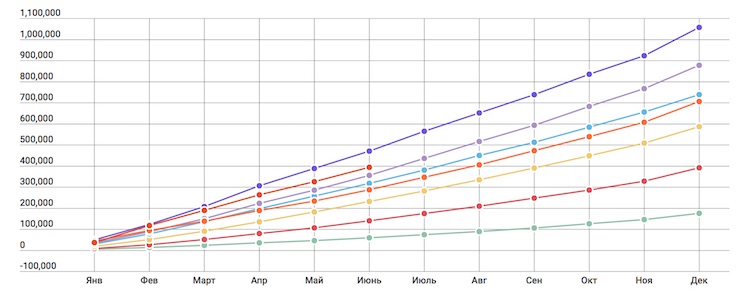

The Bank of Russia’s data about participation of non-residents in the Federal Loan Bond (OFZ) market, although seeming purely technical at first glance, permit us to reach two important conclusions. First, non-residents continue to like and to buy Russian government debt securities denominated in rubles. True, the interest accumulated from these is not very great, less than a cumulative $20 billion, but OFZ volumes in rubles are steadily growing. In other words, non-residents are continuously buying them.

Chart 5. Share of non-residents in the federal loan bond market, 2012–2016

Source: Bank of Russia

Of course, the appetite for Russian assets is not as great today as it was in 2012 and the first half of 2013, when the flow of funds from non-residents accounted for all (!) the growth of the market; but today’s share of non-residents in the market’s growth still remains significant—60–70 percent.

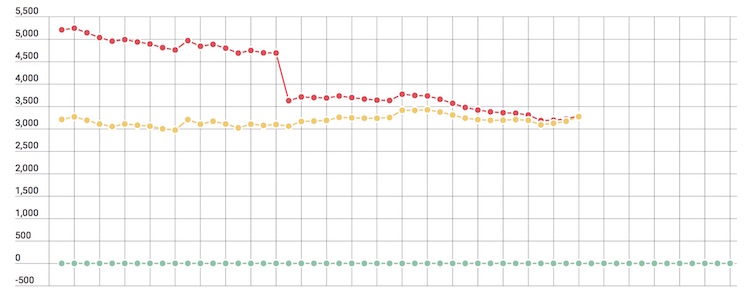

Chart 6. Volume of the federal loan bond market, nominal, with special issuances removed, 2012–2016

Source: Bank of Russia (green: volume of the federal loan bond market; red: with special issuances removed).

Non-residents aside, we must note the fact that there is no overall demand for Russian government securities. If we subtract 1 trillion rubles from the total volume of the market—the amount in OFZs issued for capitalizing banks—and another 1 trillion rubles that were provided to the Deposit Insurance Agency by the Bank of Russia for the resolution of bankrupt banks and invested in OFZs, then we understand that the peak volume in the OFZ market occurred right before the annexation of Crimea. (For purposes of drawing the chart, I subtracted the trillion for the capitalization of banks from January 2015, and the second trillion was evenly distributed over the course of 42 months from January 2013 to June 2016.)

Putting these two things together, it is easy to conclude that without the money of non-residents, the Finance Ministry would not only have no hope of attracting new assets by means of issuing new OFZs, but would also have to spend considerable tax revenue in order to retire old debts.

“There Is No Money, but You Guys Hold On”

The statement of first deputy finance minister Tatiana Nesterenko that the Russian economy is in the eye of a storm was widely disseminated and commented upon. But the second part of her statement, when she said that in the absence of reform, the government’s financial reserves will be exhausted by the end of 2017 and “the government won’t have money for salaries” went undeservedly unnoticed. Everyone already knows that the reserves will soon run out; but what happens after that?

In the first place, it should be understood that any reforms begun now can hardly produce enough of an effect that the economy will begin to grow at a rate of 10 percent per year and permit the treasury to be replenished. Even a 3–5 percent growth would not be sufficient to repay what the government already owes. In other words, the question of what to do when the reserves run out—slash the budget to the quick, or run to Neglinnaya Street (where Bank of Russia is headquartered) for money—remains unanswered. What’s more, I don’t quite understand whether the ideas of “reconciliation” with the West and a withdrawal from the Donbass belong to the concept of “reform” or not.

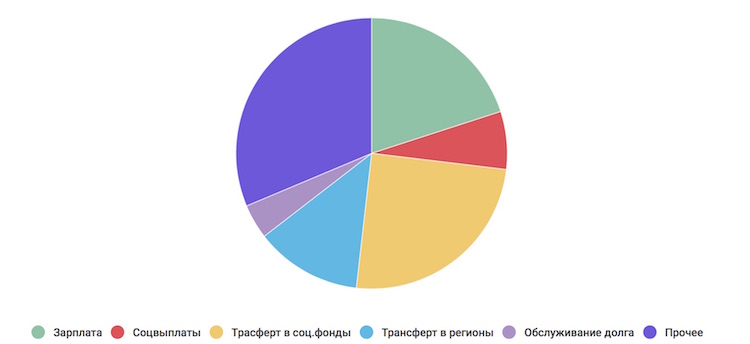

Chart 7. Economic structure of expenditures of the Federal Budget of Russia in 2015

Source: Ministry of Finance of the RF (green: wages; red: social payments; yellow: transfers to social funds; blue: transfers to regional budgets; pink: debt service; purple: other).

Secondly, and this is much more important, the statement about not having enough money for salaries is not a joke. Note what the economic structure of federal budget expenditures in 2015 looks like: 52 percent went toward direct payments to the population, and nearly 17 percent went to the regions and to interest on debts. Everything else—the rent of premises, automobiles, staples, tanks, nuclear warheads, stadiums for the 2018 World Championship Games, the Kerch Bridge, and so forth—amounted to just 31.3 percent of budget expenses. The expenditures for 2017 are not supposed to exceed this year’s, but if the decision is made to index pensions and salaries of government employees, then something must be cut. And which of the things listed above can we afford not to fund?