In his latest commentary about recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes the Russian Central Bank’s statistics for the first three quarters of 2016 and sees reason for both optimism and pessimism.

The Russian government is concerned about the ruble's stability as the foreign assets are decreasing in the country's banking sector. Photo: Artem Korotayev / TASS

Stably Unstable

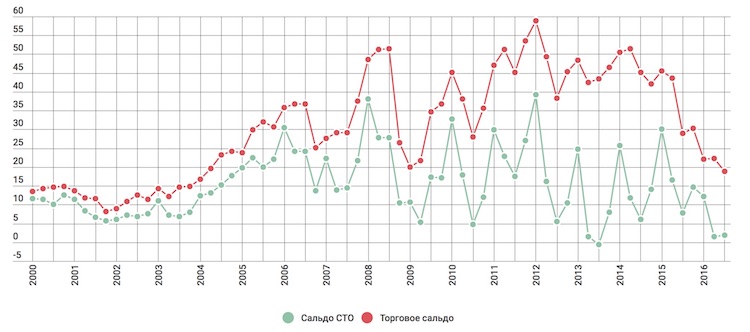

The evaluation published by the Bank of Russia of the balance of payments for the first three quarters of the current year affords sufficient basis for both optimism and pessimism. Pessimists would emphasize that the current account balance has remained close to zero for two quarters in a row, which guarantees the ruble a turbulent future. And that the balance of trade shrank by almost $10 billion, due to both a decrease in the value of exports and the growth of imports (at a ratio of 4 to 1). And that favoring the ruble was the preservation of the ban on flights of tourists to Turkey for the entire vacation season (this led to a diminished expenditure on tourist travels by $5 billion in the third quarter of this year in comparison with last).

Optimists would point out that notwithstanding the indicators mentioned above, the stability of the ruble exchange rate during the last two quarters was not only not subject to doubt, but in fact, its strengthening has begun to arouse the authorities’ concern. And that both the corporate and the financial sectors are continuing to service external debts rather smoothly, without having much access to capital markets due to sanctions.

Chart 1. Trends of Russia’s current account and balance of trade, 2000–2016 (quarterly, in billions of dollars)

Source: Bank of Russia. Green: Russia's current account; red: balance of trade.

Both are in part right. And I cannot say whose arguments are weightier. I am worried about something else. To a considerable extent, the stability of the balance of payments for the duration of the year has been maintained at the expense of the banking sector’s reduction of its hard currency assets, which have decreased by $23.4 billion in the past nine months, including $9 billion in the last quarter. In this situation we can clearly trace the “invisible hand” of the Central Bank, which successively got the banks to retire foreign currency credits received in repo operations at the end of 2014 and the first half of 2015. The Bank of Russia drove the debt level down from $20.7 billion at the beginning of the current year to $9.7 billion by the end of the third quarter.

It is unquestionably good that the Central Bank supported the balance of payments with its actions. But while banks might calmly agree to a lessening of foreign currency assets during a period when the ruble is strengthening, what will happen when it begins to weaken?

I am almost certain there will be a weakening of the ruble in the foreseeable future. The Russian economy is used to living with a large current account surplus, and its present near-zero condition is not customary. If we believe that the economy has bottomed out, then following that, there inevitably must be a growth of private current and investment demand, including for imported goods, which in the absence of a rise in oil prices will sharply change the situation on the foreign currency market.

The Pressure from Sanctions Is Weak

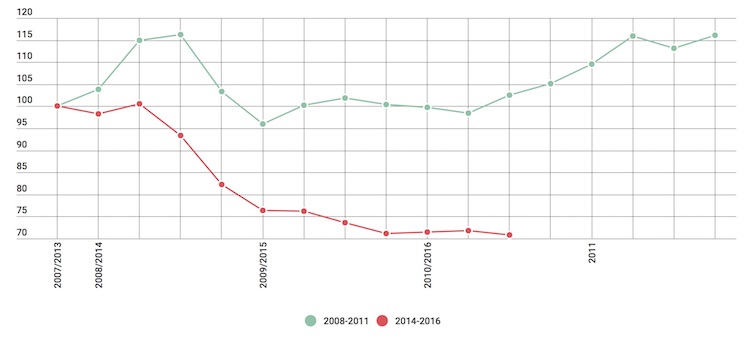

The data published by the Bank of Russia about the trend of total foreign debt (sovereign, bank, and corporate debt) as of October 1, 2016, tell us that its reduction has practically ended: at least over the course of this year, the overall amount of the debt remains at approximately the same level.

Chart 2. Trend of total foreign debt of Russia in 2008–2011 and 2014–2016 (100 = January 1, 2008, or January 1, 2014, respectively)

Source: Bank of Russia

However, considering that 17 to 20 percent of the total foreign debt is denominated in rubles, and that the Russian national currency strengthened this year against a two-currency basket by more than 13 percent, a reduction of foreign indebtedness is taking place even more intensively. Thus, in my estimate, since the beginning of the year, the total foreign debt, denominated in rubles, has lessened by approximately 500 billion rubles, but due to the growth in the ruble’s exchange rate, it has increased by almost 5 billion U.S. dollars.

From its height in the middle of 2014 ($732.8 billion) the cumulative foreign debt of Russia has decreased by almost 30 percent (in the crisis of 2008–2009 the reduction comprised 16.5 percent), but more than 80 percent of the reduction of the debt occurred during the first three quarters, beginning in the middle of 2014, after the onset of the drop in oil prices and the introduction of financial sanctions against Russia. During the subsequent six quarters, the foreign debt lessened by only $40 billion, and this is clear proof of the premise that the pressure of sanctions on the Russian economy has sharply weakened. And that today financial sanctions are no longer a determinative factor.

Good News from the Mortgage Market

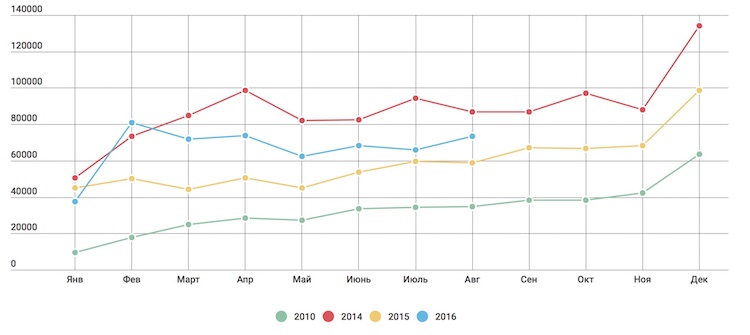

Data about the issuance of mortgage credits in August look mostly optimistic. The quantity of issued credits that month turned out to be almost a quarter higher than it was a year earlier. The share of mortgage credits received in August for the refinancing of those that had been received earlier fell just below the 60 percent crisis level. But it’s too early to say that this growth trend will continue through year’s end, as was standard for the inter-crisis period.

If the absence of growth is a consequence of distortions introduced into the statistics by increased demand for mortgages in the first months of the year, then we will inevitably see a corresponding tendency in the last quarter. And if that happens, then we can say—yes indeed – that we have passed the bottom! At least in mortgage credits.

Chart 3. Issuance of new mortgage credits in Russia, 2010–2016 (in units)

Source: Bank of Russia

If Everything Goes Well, It Might Be Better Than in 2009

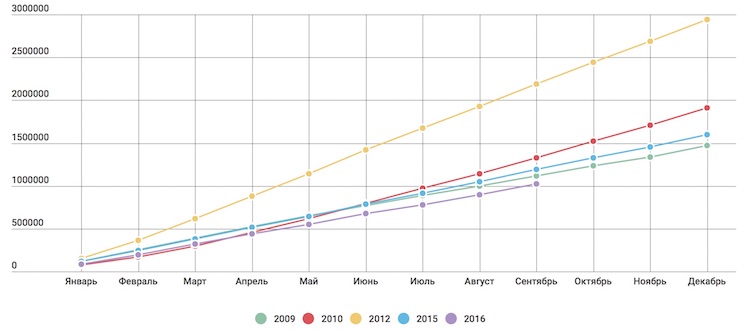

The Association of European Businesses, which keeps statistics on the sale of new cars in Russia, announced, “the market finally has surpassed the figure of one million cars. While this may not be as many as we had hoped for by this time, it is more than the pessimists had predicted for the entire year.”

Truth be told, I did not see a single forecast stating that by the end of the year the volume of sales would not exceed a million vehicles.

But in the best years for the market (2012–2014) the figure of one million was reached in May, and so far the shortfall compared to 2015 continues to grow, and the figure of one and a half million cars, which is 100,000 fewer than a year ago, is still just a dream. To reach it, it is necessary for the sales volume of new cars to be no less than it was last year for the last three months of the year. But so far each month of this year the shortfall in sales compared to 2015 can be measured in double-digit percentages.

Chart 4. Sale of new passenger cars in Russia, 2009–2016 (in units, growth from the beginning of the year)

Source: Association of European Businesses (months shown in chart: January through December).

For the optimists, I will say that in June, August, and September, the monthly volumes of sales of new cars were higher than in the same months of 2009, although the economic recovery in 2009 had already begun by summer.