In his latest article on key developments impacting the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution and former deputy chairman of the Central Bank of Russia, analyzes the latest official data and public statements, as well as manifestations of the ongoing economic crisis.

Russia's economic development minister Alexei Ulyukayev (standing) continues to play up his optimism regarding the country's economy, while prime minister Dmitry Medvedev continues to postpone the much needed reforms. Photo: Stanislav Krasilnikov / TASS

Still No Growth

Presenting his outlook of the Russian economy for 2017–2019 at the cabinet meeting last week, economy minister Aleksei Ulyukayev did not state (as he often does) that the economy had once again hit bottom and bounced back, but he still tried to sow some optimism into the audience. He stated that the “statistical results of the first quarter are better than what analysts expected, though we are still at the negative stage of the GDP growth, but the numbers are quite different from what they used to be—1.4 percent contraction [of the economy].”

I won’t fret over semantics: a rare minister masters the “great and mighty Russian language” to the point that it sounds clear and beautiful. But from his quote, I will try to extract Ulyukayev’s underlying meaning—that in the first quarter, Russia’s economy continued to slowly slide down.

Of course, the current decline of 1.4 percent looks better than the 2.2 percent that defined the first quarter of last year, but is it a cause for joy? Furthermore, the minister sees no hope of the economy returning to positive growth within the next two quarters at least, which means that in the best case scenario, the recession will have lasted for nine quarters in a row.

No Reforms Either

Prime minister Dmitry Medvedev’s speech at the State Duma might have flown under my radar if it hadn’t been for one statement that caught me off-guard: “Yes, the country needs deep structural reforms. The government understands this perfectly, but it also understands how [these reforms] will reflect on the social sphere. Any forceful transformations would have strengthened and prolonged crisis developments for several years. Therefore, I’d like to say... that we will not conduct any reforms at the expense of the people.”

One can only conclude from this quote that the only structural reform the Russian prime minister is familiar with is pension reform, or, to be more precise, the idea of raising the retirement age. Consequently, the prime minister is discussing neither liberalization of the gas market, nor free access to the pipeline transportation business, nor real privatization and the state’s withdrawal from competitive sectors of the economy (what Putin promised to do in his May 2012 decrees), nor reforms to law-enforcement or the judiciary. In other words, all the areas where there would be no need to implement reforms “at the expense of the people” were disregarded.

At the Duma the prime minister also stated that no change will be made to the federal budget during the spring session or after, until the current parliament’s powers expire in the end-summer session. What this actually means is that additional indexation of pensions has been ruled out for this year. One can understand the government’s decision: it would be politically correct to increase pensions before the elections, but only by three to four percent, which pensioners may perceive as a cruel joke. Thus, it’s better to scrub the topic from the agenda.

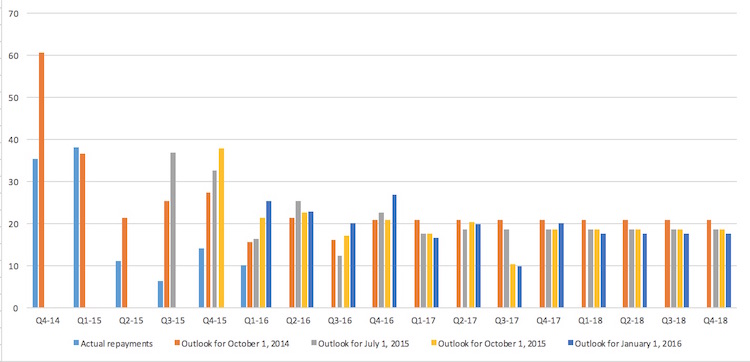

On Foreign Debt

Bank of Russia published its outlook for upcoming foreign debt repayments as it stands on January 1, 2016. And once again, this outlook made me seriously question the official numbers. The bank’s experts have been steadily increasing their estimates for the amount to be repaid in the first quarter—up to their current estimate of $25 billion. But in reality, actual repayments during the first quarter turned out to be slightly less than $10 billion. The conclusion the regulator (Bank of Russia) is drawing based on these numbers sounds familiar: there will be no “peak” repayments in the coming two years; thus the pressure of financial sanctions will be quite uniform.

Chart 1. Outlook for upcoming repayment of Russia’s foreign debt, in $ billions per quarter

Source: Bank of Russia

On the Crisis

It’s difficult to gain a clear picture of what’s happening in the Russian economy, since its dominating sector is energy exports, but domestic production data is extremely distorted by the results of the defense sector. One needs to be on the lookout for indirect indicators that can shed some light on the situation.

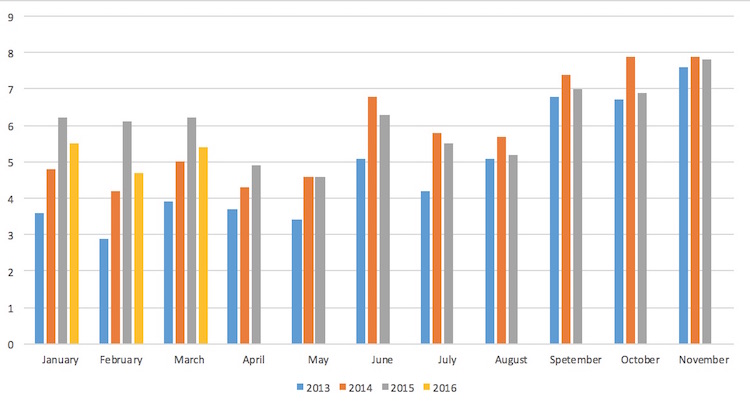

Currently, I suggest looking at the dynamics of residential construction—a sector that uses domestically produced materials and, in many ways, reflects more general domestic demand trends. Rosstat data on the introduction of residential properties points to the fact that in the first quarter, their volume decreased by 15 percent compared to the same period last year.

Of course, one might say that the beginning of the year is a low season, and that introduction of new residential properties in December can easily exceed first-quarter results. Yes, it’s true. But I think the situation is too serious to dismiss these indicators.

During the previous crisis, despite mass bankruptcies among developers, the volume of residential construction decreased at a very small rate. The market dropped by only 9 percent in December 2009 and the second half of 2010 (relative to the 2008 level). Clearly, the current drop in household incomes and collapse of mortgage market demand led to the decrease in co-financing of residential construction. Thus, one should not expect a fast recovery of the households’ investment potential.

Chart 2. Introduction of residential properties to the market in Russia, 2013–2016, month-to-month (in millions of square meters)

Source: Rosstat