In his latest commentary about recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes Russia's economic results for May, and once again finds no good news.

Russia's Minister of Economic Development Alexei Ulyukayev seems to be perpetually looking for the "bottom" of the Russian economy. Photo: Alexei Druzhinin / TASS

If Pigs Could Fly

Economic Development Minister Aleksei Ulyukayev was again incorrect in predicting the bottoming out of the Russian economy. The country’s economic results for May were so disappointing that not only was he forced to admit that things are going badly, but his deputy Aleksey Vedev found it necessary to publicly criticize the experts at the Center for Development, who “exaggerated” the situation by assessing May’s results at -0.7 percent for the month.

Whether they exaggerated or not is a subjective question: is the glass half empty or half full? However, May’s statistics contain no good news—that’s a fact.

Three months ago Rosstat’s estimates left room to hope for a positive turn in the population’s real income, which would have been followed soon afterwards by the start of growth in private consumption. Now it seems Rosstat’s winter estimates were flawed, seriously distorting reality. The strongest evidence of this is the persistent drop in retail trade, testifying to the public’s ever-shrinking consumption, which has declined almost 15 percent over the last two years.

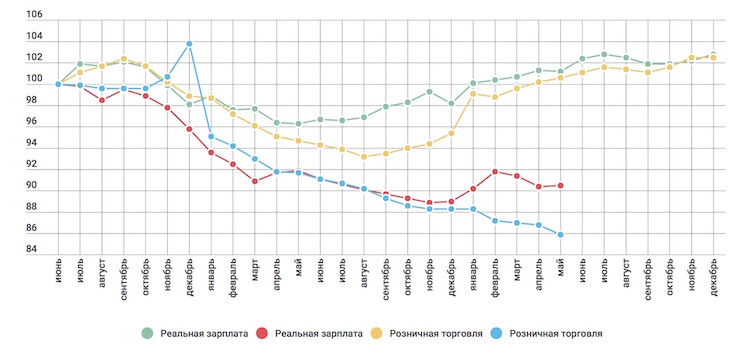

Chart 1. Trend of real wages and retail goods turnover in Russia, 2008–2010 and 2014–2016, seasonally and calendar adjusted) (10 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development (green — real wages, yellow — retail, 2008-2010; red — real wages, blue — retail, 2014-2016).

The second unpleasant fact in the May statistics was about the trend in construction work (remember, Rosstat stopped publishing monthly estimates of investment, switching to quarterly reporting): this data showed a worsening falloff.

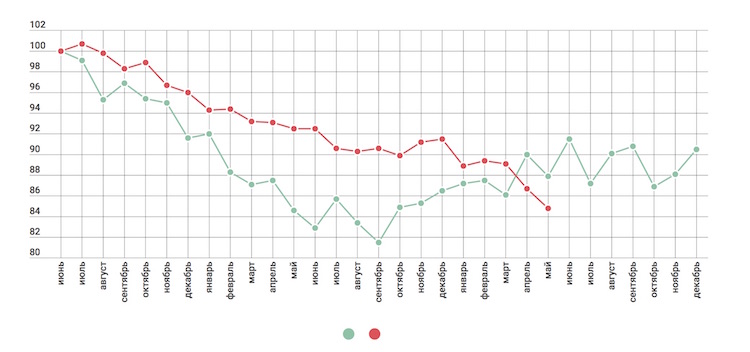

Chart 2. Trend of construction in Russia, 2008–2010 and 2014–2016, seasonally and calendar adjusted (100 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development (green — 2008-2010, red — 2014-2016).

Minister Ulyukaev appraised the May results as a fall of 0.8 percent per annum, which is less than the cumulative decline in the economy since the beginning of the year (1 percent per annum). This did not change the forecast of the Economic Ministry, which promises that by the end of the year there will be only a 0.2 percent fall in GDP. In other words, “The bottom—if it hasn’t been reached—will surely be reached!”

One would like to believe it.

The Engine Is Definitely Not Working

Just as clearly as they showed that economic bottom has not been reached, the May statistics confirmed that the two motors of the Russian economy—the raw materials sector and the military-industrial complex—are running without a hitch. Both sectors continue to grow, which keeps railway transportation afloat.

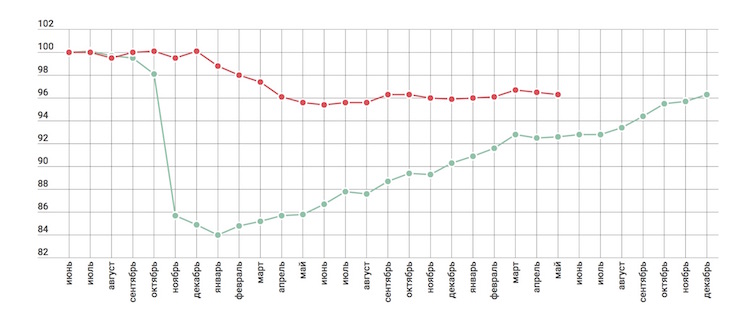

Chart 3. Trend in Industry in Russia, 2008–2010 and 2014–2016, seasonally and calendar adjusted (10 = June 2008 = June 2014)

Source: Rosstat, Adjustment: Center for Development (green — 2008-2010, red — 2014-2016)

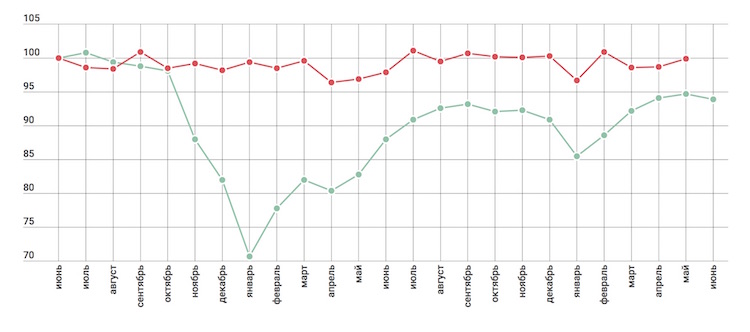

Chart 4. Trend in rail freight turnover in Russia, 2008–2010 and 2014–2016, seasonally and calendar adjusted (10 = June 2008 = June 2014)

Source: Rosstat. Adjustment: Center for Development (green — 2008-2010, red — 2014-2016).

That is the only positive news, though. The power of these motors is clearly not sufficient to make industry as a whole (let alone the economy as a whole) begin to grow. The charts clearly show that the most these motors can do is keep industry as a whole from plunging.

We know that the share of the raw materials branch in industrial production comprises 36 percent, and that it grows at a rate of 1 percent per year. Rosstat does not tell us the share of the defense industry—apparently they’re afraid that if Russia’s enemies learn it, they will learn the dark secrets of the tactical and technical characteristics and distribution of the latest Russian weaponry. But if we assume that it comprises 15 percent, and military production grows at a rate of 15 percent per year, then it turns out that the rest of industry is declining by 5 percent per year. But there are other growing sectors, our government assures us!

Who Has It Good These Days?

In an inertly falling economy the banking system can hardly do well—the latest information from the Bank of Russia confirms this. Since the beginning of the year, the basic indicator of banking activity—credits to the economy—has not grown at all. Growing deposits by the public help banks to do without expensive credits from the Central Bank (both ruble-denominated and foreign currency ones) and to extinguish foreign debts, which is undoubtedly good. But this doesn’t influence economic growth at all: the banking sector doesn’t want to support the real sector. Or it simply doesn’t see how it can.

What Is the Bank of Russia Afraid of?

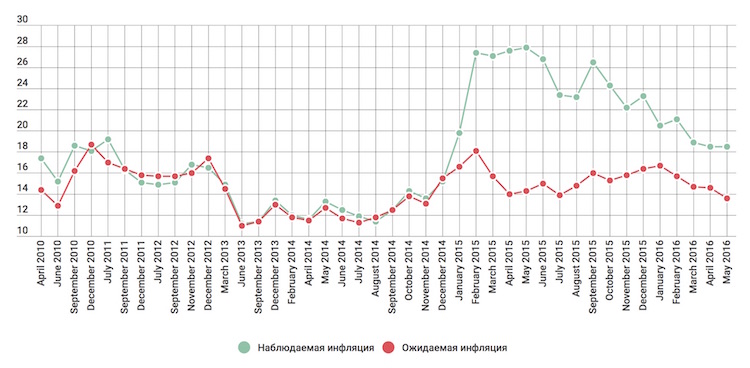

Behind schedule due to its board of directors’ discussion of the issue of lowering rates, the Bank of Russia published its estimates of the inflation trend and the public’s inflation expectations. There was nothing unexpected there—both indicators continue to decline in the wake of current inflation, although it would be difficult to call their levels normal for an economy with falling demand.

I was personally glad that inflationary expectations of the public have been falling for four months in a row now. However, the fact that the general level of those expectations remains rather high, and that the gulf between the estimate of current inflation and expectations has stopped lessening, speaks to the fact that the public remains concerned and does not fully believe the promises of the Central Bank that it will still further slow the growth in prices.

The next three months will be very important for the current year’s inflation trend. On the one hand, there is a forthcoming indexation of utilities rates, which will objectively worsen the statistics. On the other hand, summer horticultural deflation may be smaller than usual due to the weak growth of prices in horticultural goods this spring (experts at the Bank of Russia note this in their summary). We should also not forget that the ruble traditionally weakens during the August–September period, and even a rather weak devaluation of the ruble can heat up inflationary expectations.

Chart 5. Direct estimate of inflation and inflationary expectations of the public for the next 12 months (%)

Source: Bank of Russia (green — сurrent inflation, red — expected inflation).

There remains a full month until the next meeting of the Board of Directors of the Bank of Russia, which will review the decision about the key rate. But June statistics on inflation and inflationary expectations will certainly be the major factor to determine their decision.