In his latest commentary on recent events in the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes statistics for the Russian economy through the first half of the year and finds the results are worse than expected. He also discusses the Kremlin’s nervousness concerning the strengthening of the ruble, and notes that the reduction of the net amount of trade operations in the balance of payments is causing still more alarm, and under current conditions could lead to rapid devaluation of the ruble.

Vladimir Putin's aide Andrei Beloussov has recently claimed, in support of the view voiced by the presindent, that strengthening of the rube is apparently bad for the economy. Photo: Mikhail Klimentyev / TASS

Things Got Worse

The full statistical summary that came out at the end of June summarized the first half of the year, and things were worse than expected. The Economic Ministry and the Development Bank have not given their estimates for June, and the Center for Development notes a progressive fall in domestic private demand accompanied by relative stability in the trend for key sectors.

Chart 1. Trend in Basic Sectors and in Final Domestic Private Demand in Russia in 2008–2016, seasonally and calendar-adjusted (100 = 2010)

Green: final domestic private demand; red: basic sectors.

Source: Center for Development of the Higher School of Economics National Research University

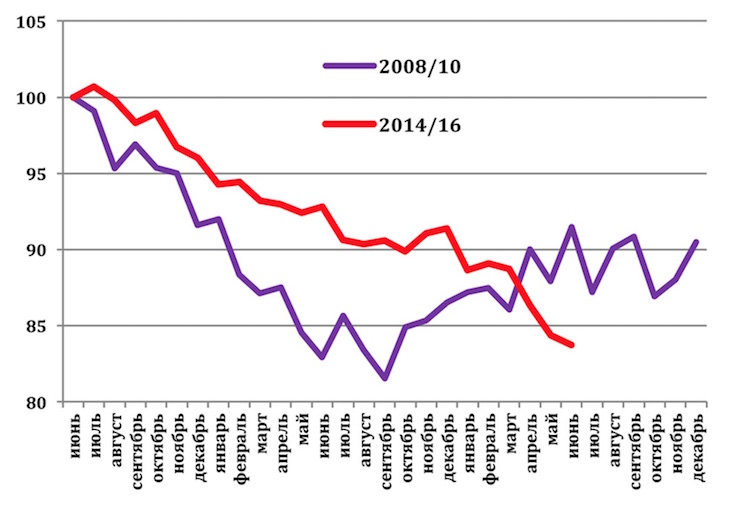

Chart 2. Trend in Construction in Russia from 2008–2010 and 2014–2016, seasonally and calendar-adjusted (100 = June 2008 = June 2014)

X-axis: monthly indicators measured from June 2008 through December 2010 (purple line), and from June 2014 through June 2016 (red line).

Source: Rosstat. Adjustment: Center for Development of the Higher School of Economics National Research University

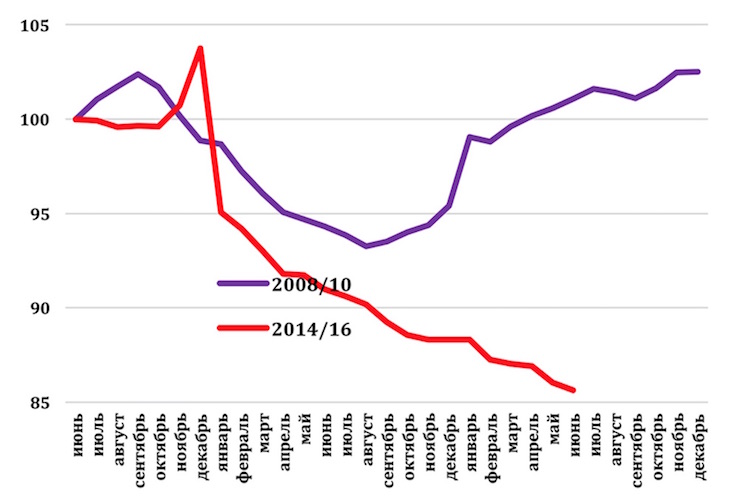

Rosstat’s findings inspire little optimism about all three components of domestic demand: the budget is not even worth mentioning, and the Finance Ministry’s policy aimed at reducing expenditures will inevitably lead to contraction of government demand; relative to last year, construction as a whole (as an approximation of investment) was falling more rapidly by the end of the half-year, although it must be noted that the housing construction results for June exceeded last June’s figures; and the turnover in retail trade continues to head downhill—although the fall in real incomes of the population has almost stopped, it is likely that the latter indicator fails to show that the incomes of the lower- and middle-earning segments of the population continue to fall rapidly.

Chart 3. Trend in retail trade in Russia in 2008–2010 and 2014–2016, seasonally and calendar-adjusted (100 = June 2008 = June 2014)

X-axis: monthly indicators measured from June 2008 through December 2010 (purple line), and from June 2014 through June 2016 (red line).

Source: Rosstat. Adjustment: Center for Development of the Higher School of Economics National Research University

The Problem With the Budget

Vladimir Putin’s unexpected declaration that something must be done about the strengthening ruble came like a bolt out of the blue. An explanation of the president’s statement followed from his aide Andrey Belousov, who said bluntly: “Today the ruble is beginning to strengthen again, and this has negative consequences, by which I mean that it is lessening budget income and worsening the budget problem.” In other words, the Kremlin blames the overvaluation of the ruble on the lowering of oil and gas income in terms of the ruble equivalent. This sounds strange to me.

Really, the budget situation is lousy. And the Finance Ministry’s data about the implementation of the federal budget for the first half of the year shed a lot of light on the nervousness that has taken hold of the Kremlin. For the first half-year, the flow of oil and gas revenue amounted to only a little more than a third of that planned for the year. If oil and gas income for the second half of the year comes in according to plan and the remaining income for the year is not lower than established in the law on the budget, then the year-end federal budget deficit will exceed the planned level by more than 50 percent (2.6 trillion rubles versus 1.7 trillion rubles).

But the Kremlin reaches a strange conclusion based on this: since we can’t influence world oil prices, they say, it is the overvaluation of the ruble that is to blame for the shortfall in income! Yes, of course, if one could wave a magic wand and weaken the ruble by some 10 percent, this would almost automatically lead to an increase in budgetary income, but “almost” is the operative word here.

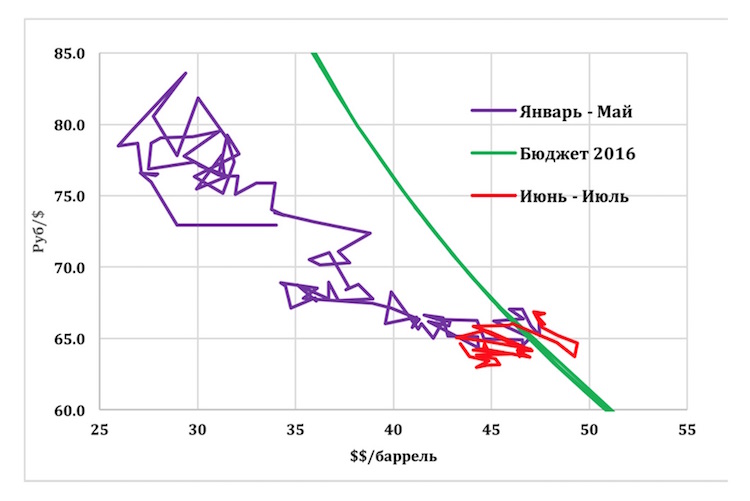

In the chart below, the green line indicates which paired values of the export price for Russian oil and the exchange rate of the ruble attain the exact value (3,050 rubles per barrel) that is contained in the budget. Accordingly, if the real values are located to the right of the green line, then there will be additional budget income, and if to the left, a shortfall. And this chart demonstrates very well that over the last month and a half (June–July) the ruble price of oil has been very close to the planned one, and at times has even exceeded it. By contrast, in the first months of the year, especially in January and February, when world oil prices were at a local minimum, the ruble price of oil was much lower than planned. In order to maintain a good budget situation when oil prices were $29 to $30 a barrel, the exchange rate of the ruble would have had to drop to 105 to 110 rubles to the dollar, whereas in fact it stood at around 83 rubles to the dollar.

Chart 4. Change in price of Urals oil ($/barrel) and exchange rate of the ruble (rubles/$) in 2016

Purple: ruble price of oil in January-May 2016; red: ruble price of oil in June-July 2016; green: the exchange rate (rubles/$) needed to maintain a good budget.

Sources: Bank of Russia, Bloomberg

The explanation for this is simple: the Russian economy adapted much more quickly to low oil prices than it was expected, and, given oil prices in the range of $30/barrel, to achieve a stable balance of payments (BOP), an exchange rate for the ruble of 75–80 rubles per dollar was quite sufficient. For the economy, but not for the budget. However forcefully President Putin hinted at the overvaluation of the ruble, it is clear the market won’t take this seriously: the ruble’s exchange rate can be lowered either by the Central Bank with its massive ruble interventions, which it has no intention of doing, or by a sharp surge in demand for imported goods and services, which is more likely.

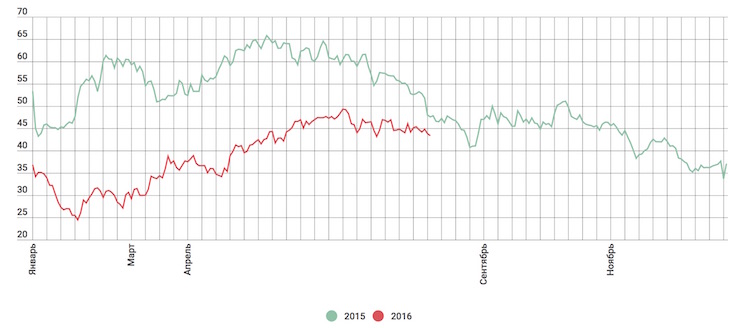

Chart 5. Change in Urals oil prices ($/barrel) in 2015–2016

Sources: Bank of Russia, Bloomberg

On the one hand, the BOP net current account balance contracted to a minimal level (more about this below); on the other hand, the opening of the Turkish resorts to Russian tourists after the travel ban was lifted will lead to growing public demand for foreign currency. Moreover, we mustn’t forget that August/September is traditionally a season of increased demand for foreign currency on the domestic market.

If we add the slowly but steadily dropping price of oil, then a rapid weakening of the ruble over the next two months seems like a realistic scenario.

But I don’t think the Kremlin will be too happy about this. If oil gets cheaper to the extent that it did last year, the devaluation of the ruble (by analogy with last year) could be substantially less, and the shortfall of budget income will be all the more significant. And if the devaluation of the ruble were very great (15 to 20 percent), doubtless this would lead to more rapid inflation.

To sum it up, I’d say the president really shouldn’t have brought up the subject! As they say, let sleeping dogs lie.

In the Zone of Instability

I don’t want to be an alarmist, but it seems to me that the Russian BOP has entered a zone of instability. I realize this may sound strange given the monotonously strengthening ruble, but “Plato is my friend, but the truth is a better friend!”

At the end of the second quarter of this year, the BOP net current account balance was reduced to $2.4 billion dollars, which comprises less than 1 percent of GDP. If we look at the history of the Russian economy over the last 20 years, each time this figure dipped below 1.5 percent of GDP, the ruble sharply lost value. You might very well ask: what about 2013, when we made it through without devaluation? The thing is, Elvira Nabiullina, who assumed the position of chairman of the Bank of Russia in the middle of that year, felt she couldn’t permit devaluation to begin during the first days of her chairmanship, and issued an order to conduct a massive sale of foreign currency, which lasted from June 2013 to the beginning of May 2014. This helped prevent devaluation, but cost the Central Bank about $50 billion dollars (10 percent of foreign currency reserves).

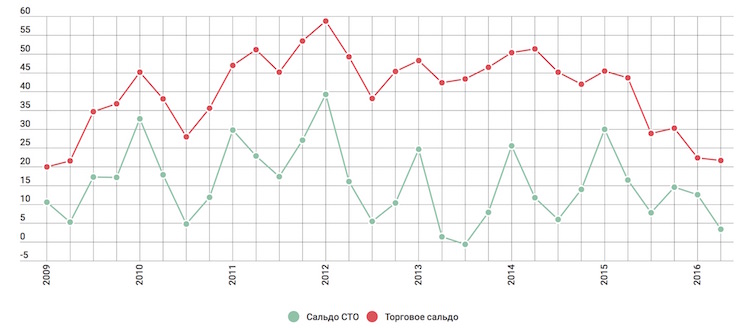

A rapid reduction in the balance of trade makes the BOP situation still more alarming.

This means that a sudden reduction in earnings from the export of goods is compensated for not by a corresponding reduction of imports, but by a reduction of other current expenditures (services, salaries, dividends, etc.).

Today, it seems, the Bank of Russia won’t attempt currency interventions for the sake of supporting the ruble’s exchange rate—especially given the president’s desire to do something about its strengthening—and will calmly watch as the ruble cheapens by the day. Keeping in mind that seasonally, the ruble tends to weaken as summer turns to fall, a 10 to 15 percent devaluation of the ruble wouldn’t surprise me.

Chart 6. Russia’s BOP net current account balance and balance of trade ($ billions/quarter), 2009–2016

Green: BOP net current account balance; red: balance of trade.

Source: Bank of Russia

Two Surprises

The Bank of Russia’s published estimates for BOP and forthcoming payments on the debt have brought two bits of unexpected news. First, it turns out that in the second quarter, Russian banks and companies were able to become pure borrowers in operations with debt. And although the amount isn’t great ($2.2 billion), it means that the pressure of financial sanctions in the second quarter was reduced to nothing.

Chart 7. Estimate of forthcoming payments for extinguishing foreign debt and actual payments ($ billions/quarter), 2009–2016

Red: estimate, October 1, 2014; blue: estimate, January 1, 2016; green: estimate, April 1, 2014; blue line: actual payments.

Source: Bank of Russia

Secondly, in the first quarter of 2018, a local maximum of payments toward repaying foreign debt—a bit less than $30 billion, shows up unexpectedly, although just three months ago this amount was less than $18 billion. Clearly, one and a half years is quite some time, and the amount of repayment over this time could change in any direction. Therefore, no predictions should be made, but it doesn’t hurt to take note of this debt situation.