In his latest commentary about the recent events in the Russian economy, Sergey Aleksasheko, nonresident senior fellow at the Brookings Institution, notes that the Bank of Russia’s decision to raise the key rate will have no effect on the economy. Rosstat’s new methodology, which unexpectedly bolstered last year’s Russian economic indicators, also raises questions in his mind.

Russia's Minister of Economic Development Maxim Oreshkin (above) has publicly accused Rosstat of incorrect implementation of the seasonal and calendar adjustment during the revision of last year's economy data. Photo: Sergei Fadichev / TASS.

The Decision Has Been Taken, But There Will Be No Effect

The Bank of Russia has finally admitted the obvious and summoned the resolve to lower the interest rate. I say this without any irony—after all, the dogmatic approach to monetary policy that prevails today in the Kremlin sought to keep the rate at an unreasonably high level for another month or two. True, it must also be noted that lowering the rate by 0.25 percentage points will not have any effect on the economy. The current rate of inflation is decreasing rapidly, so we should not expect a revival of demand for credit or a recovery of economic activity, in my view.

The Board of Directors of the Bank of Russia will next consider the issue of the interest rate at the end of April, and I would be ready even now to guess that there will be one more lowering, if it weren’t for one thing . . . That spring is the period of seasonal excess of foreign currency supply over demand on the Russian currency market. If we look at history, then we see straight away that at this time the Bank of Russia has very often increased its foreign currency reserves. So we should not be surprised that the price of oil at the beginning of the month dropped by 10%, but the ruble clearly wants to strengthen.

In such a situation the monetary authorities are faced with a difficult choice: either to continue the policy of letting the ruble float freely, allowing the national currency to strengthen, let’s say to 52-53 rubles per dollar, or to consider that such a strengthening of the ruble is undesirable and to begin purchasing currency, thus increasing the monetary supply. In the first scenario, the lowering of the rate would be highly probable, but in the second scenario the Bank of Russia would have to intensify its efforts to sterilize ruble liquidity and thus not permit a lowering of its deposit interest rates, which as of today are determinative when the decision to set the rate is made.

In short, the Bank of Russia needs to grapple with finding an answer to the question, “Who should we listen to more? The Ministry of Finance and the Ministry of the Economy, which categorically demand a weakening of the ruble (the one for increasing budgetary income, the other for supporting import substitution), or the economy, the revival of which is being hindered in no small part by the high interest rates and the credit contraction.”

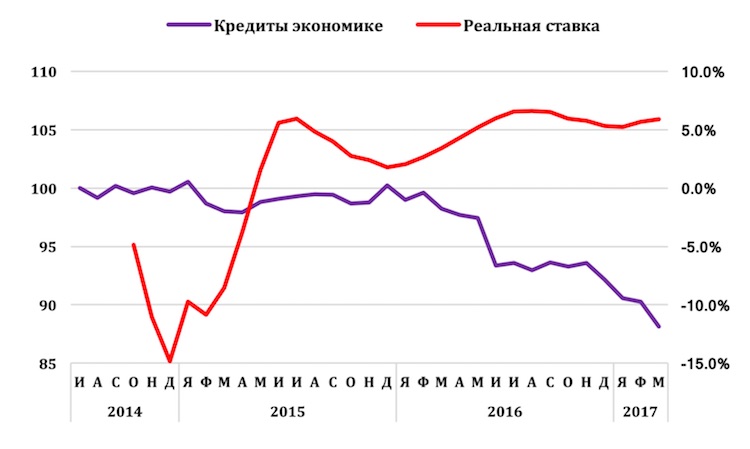

The chart below clearly illustrates how quickly the volume of loans provided by the Russian banking system to the economy has begun to fall since the beginning of 2016, and how it corresponds with the rapid growth of the real interest rate. Since the middle of 2016 we have seen the real rate remain at a level of more than 5%—the Bank of Russia has termed this a moderately austere policy which, to judge by the statement of Elvira Nabiullina, the Bank intends to carry out over the span of “the next two to three years.” If this does happen, then the Bank of Russia’s economic growth prediction (1-1.5% in 2017-2018 and 1.5-2% in 2019) might be the rosiest possible forecast.

Chart 1. Dynamics of loans to the economy (100= July 1, 2014) in real percentage rate [1]

Source: Bank of Russia (red line: effective rate; purple line: loans to the economy).

[1] For assessing the dynamics of lending to the economy, ruble loans are weighted by share and inflation adjusted, and currency loans were used. The real percentage rate is calculated as the difference between the key rate of the Bank of Russia and cumulative half-year inflation (3 months before, and three months after the reference date).

Political False Start

The publication of Rosstat’s economic data for February favors my hypothesis that the economic revival reported by all ministers late last year and early 2017 was the result of a great job by the Rosstat team.

For the highly qualified statistician, it is not especially difficult to improve the indicators for the last period, if you let him “play” with the composition of the basket and the weights of the separate components that go into it. Improving the past (in the sense of an Orwellian re-writing of history) has an obvious beneficiary, which on the eve of the upcoming election could confidently declare that under its wise leadership the country has emerged from the crisis.

However, improving the past creates obvious problems for those whose job it is to come up with a forecast. It is no secret that any economic forecast is based on an extrapolation from prior trends. Therefore, if the economy began to grow in 2016, then in 2017 this growth trend should strengthen, which should lead to a more optimistic outlook.

But any expert well understands that a simple increase in the base leads to a slowing of the growth trend, or to its disappearance, which indeed occurred at the beginning of this year. It is possible, of course, to behave like Minister of the Economy Maksim Oreshkin, who publicly accused Rosstat of having distorted the seasonal and calendar adjustments. However, I think the problem lies elsewhere. I don’t know who pushed Rosstat toward the changes in methodology which improved the results for 2015-2016, but clearly these people didn’t confer with the Department of Domestic Policy of the Kremlin administration. The latter know that on the eve of the election, instead of raising the results for 2016, it would have been better to lower them, taking advantage of the base effect in the right direction and demonstrating economic growth in the run-up to the March 2018 vote. But it turned out to be a false start…

The Budget and Oil and Gas Income

At first glance, the situation with the federal budget shouldn’t cause alarm: higher than forecasted oil prices ensure the treasury a sufficient income level. Moreover, the Ministry of Finance believes that there is too much of it and is using the above-target amount to purchase foreign currency. At the same time, the situation is far from rosy. After all, how could it be in a stagnant economy?

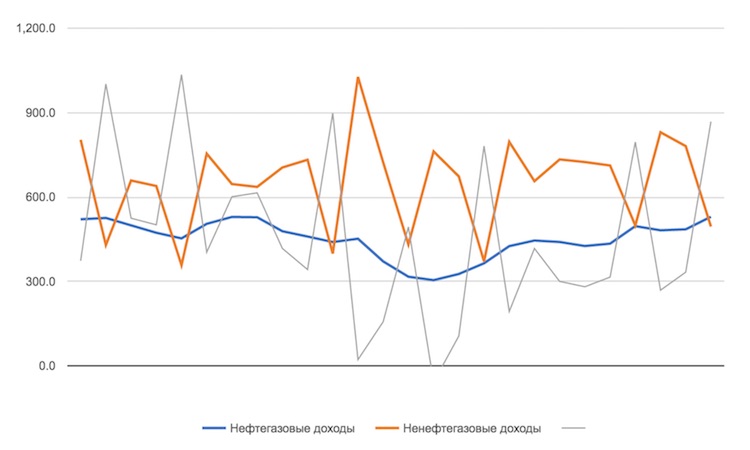

The fact that the Russian economy is stagnating is quite evident from Chart 2. The non-oil-and-gas income dynamics (reduced by the proceeds from the sale of Rosneft shares) have not demonstrated the least positive trend since the end of 2015, even in real terms, without adjustment for inflation.

Chart 2. Monthly income of the Russian federal budget, 2015-2017 (billions of rubles)

Source: Ministry of Finance (blue line: the oil-and-gas income; orange line: he non-oil-and-gas income).

One last bit of news: the share of oil and gas income in the overall volume of federal budget revenue (a sliding three-month average), which a year ago was below the 35% mark, has now exceeded 42%. Of course, the figure of 50% or more, which was the “norm” up until the middle of 2014, is a long way off, but the fact that fiscal dependence on the price of oil is again on the rise is worthy of attention.

The original Russian version of this article has been edited for clarity.