In his latest comment on key developments impacting the Russian economy, Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution and former deputy chairman of the Central Bank of Russia, analyzes the foreign trade dynamics and implementation of the federal budget for January, noting that the general outlook remains grim.

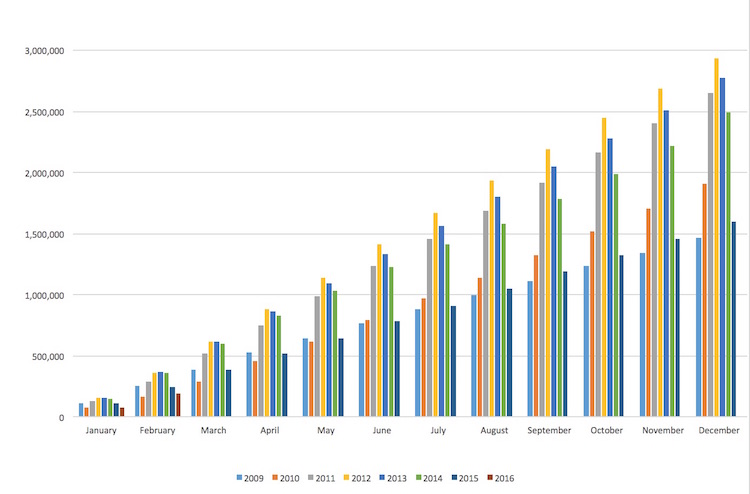

Two months into the new year, Russia has already seen a 20 percent decrease in car sales compared to early 2015. Photo: Mikhail Dzhaparidze / TASS

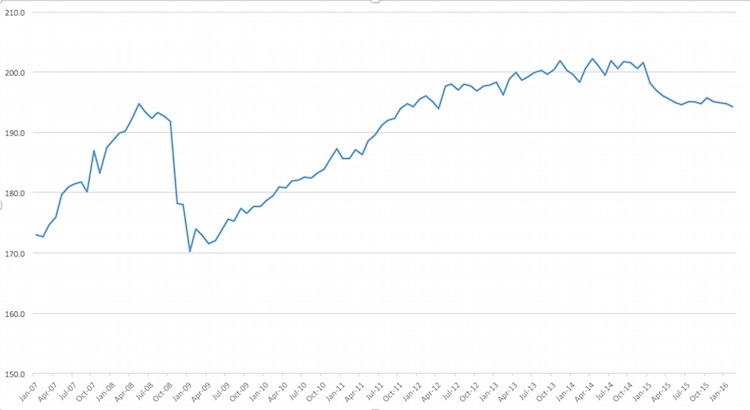

Experts from Russian development bank Vnesheconombank (VEB) have analyzed Russia’s economic dynamics for January, and their conclusions confirm an earlier outlook—the economy is failing to stabilize and return to growth. In other words, the economic downslide continues. It will be interesting, however, to see the dynamics for March and April, when the data will reflect the current hike in oil prices.

Chart 1. VEB’s GDP outlook (January, 1999 = 100, not adjusted for seasonal and calendar factors)

Source: Vnesheconombank

Exports and Imports Decline

Bank of Russia has also published its foreign trade outlook based on dynamics for January. The decline in exports (down by 34.6 percent compared to January 2015) was to be expected in light of decreased oil prices. Russia’s export value has already fallen below its 2006 level, but it’s still too early to call this a disaster. For one thing, the export value in January equaled that of the first quarter of 1998, so the economy has been through worse. For another, unlike in January 2009, the current decline is not about a drop in the physical volume of export, which explains the relatively stable state of the economy.

Import costs declined much less in January (down by “only” 21 percent compared to January 2015), and this will have rather serious consequences.

A good example of how a decline in imports influences the consumer market can be found in the drop in new car sales in Russia this February. Last fall I predicted we might see signs of market stabilization or even weak growth. Alas, we can forget about that today: two months into the new year, we’ve seen a 20 percent decrease in car sales compared to early 2015.

Chart 2. New car sales in Russia (total number of cars sold since the beginning of the year), 2009–2016

Source: Association of European Business

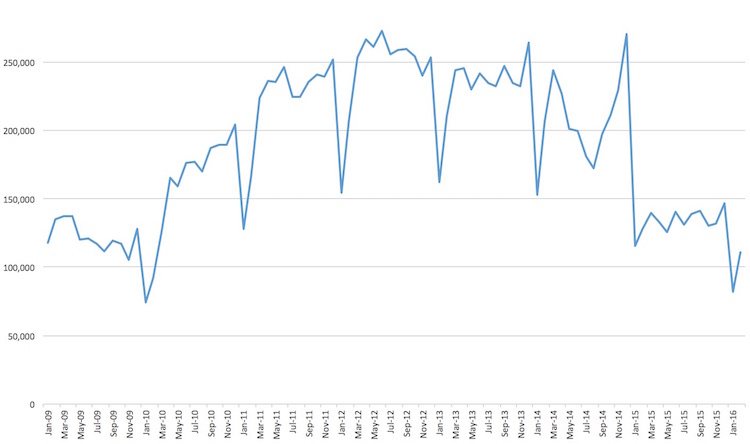

Chart 3. New car sales in Russia (month-over-month), 2009–2016

Source: Association of European Business

The situation might change slightly when the government relaunches its program of subsidizing car loans rates, but that would only slow the downslide. It seems we should no longer expect market growth this year: after the 2008–2009 crisis, the market had recovered by spring 2010—about nine months after people’s real incomes hit their lowest point. Today, we’ve still yet to reach bottom, and hardly any expert can say with certainty when (and why) this might happen.

Under such circumstances, it should come as no surprise that international car manufacturing companies might decide to shut down their assembly facilities in Russia. Chances of turning a profit in the country are growing very slim.

Budget Not Feeling Well…

February statistics on implementation of the federal budget yield two pieces of news—one good, one bad.

The good news is that the Finance Ministry managed to balance expenditure financing, which means that if monthly spending stays at its current level until the end of the year, December “peak” spending might be reduced. Moreover, the January pause in military spending did not last long, and in February the defense sector received everything it was supposed to according to the budget. Today, of course, there are no advance payments for arms procurement like last year, but as of now there have been no spending cuts either.

The bad news is that February spending decreased by 22 percent compared to last year (overall, a 19-percent decrease over the last two months). The major factor impacting the situation is a rapid decline in oil and gas revenues in the federal budget: mineral resources extraction tax revenues (MRET) fell by 42 percent in February, and hydrocarbons export duty revenues decreased by one-third. Over the last two months, oil and gas revenues have fallen by one-third as well (compared to the same period last year), and their share has shrunk to one-third of the total federal income—it was 54 percent in 2013. Against this background, one wants to believe that the current collapse in domestic income (from collecting the value-added taxes and excise taxes that dropped by 31 percent and 23 percent, respectively, compared to February 2015) is only temporary and that it will be compensated for by the January hike in the respective tax revenues (which increased by 39 percent and 56 percent, compared to January 2015).

…Neither is the Nickel Market

Along with the oil market, the nickel market is another important sector of the Russian economy that’s facing a supply glut. Norilsky Nickel Vice President Pavel Fyodorov estimates that the excess is about 25 percent—which, he notes, explains the 40-percent drop in nickel prices last year. Fyodorov says that 70 percent of global nickel output will be loss-making at current prices, but this trend will not affect his company, which still plans to generate profit.

Clearly, the importance of Russian nickel exports can’t be compared to that of oil and gas, but the decrease in Norilsky Nickel’s financial flows is inevitable, and it will further contribute to declining demand in the Russian economy.

Defense Cuts?

The current critical condition of federal budget revenues has forced Russian authorities to make decisions that seemed impossible just two months ago. According the the latest statements by the head of the state corporation Rostech, Sergei Chemezov, the government’s defense order might be cut by 10 percent this year. Chemezov said that the cuts would not affect work that has already been initiated—but they will be applied to projects scheduled to start within the year.

This means that accounting for a two-to-three-year cycle in armaments production, by 2018–2019, Russia’s military-industrial complex (MIC) might face a serious slump in production levels. One has to keep in mind that starting in 2018, additional state procurement cuts are planned for many items—something that could cause employment issues at MIC factories and the deterioration of their financial health.