In his latest comment about recent events in the Russian economy Sergey Aleksashenko, nonresident senior fellow at the Brookings Institution, analyzes the latest interview with Elvira Nabiullina, head of the Bank of Russia, highlighting obvious contradictions within it, and also looks at the economic indicators of the last few months and finds reason for restrained optimism.

Nabiullina's Credo

The widely cited interview with the chairman of the Bank of Russia, Elvira Nabiullina, devoted to issues of monetary policy, is indeed worth taking note of. I would call attention to four basic points in it.

- It is confirmed that the Bank of Russia intends to “anchor” inflation and inflationary expectations at the level of 4%. I repeat in this connection that this is a mistake, as such inflation is high by current global standards, and the Bank of Russia should achieve a lower rate of price growth.

- It seems to me that this is the first time that the Bank of Russia has issued guidelines for the level of real rates of interest: a range of 6.5%-6.75% was mentioned with inflation at 4%. Hence, according to Nabiullina, the Bank of Russia has sufficient leeway for lowering the key rate. Such news is welcome, because the ultra-harsh policy of the Central Bank continues to suppress the demand of the economy for credit. In my opinion, a level of 2.5%-2.75% for the real rate is nonetheless somewhat high, and I would prefer to hear about 2.5% today with a subsequent lowering to a level of 1.5%. But this is obviously better than the 5% real rates which we have today. However, let's not forget that all my assessments and judgments in this case relate to the key rate of the Bank of Russia, but the real rate for corporate credit in Russia (to judge by the Central Bank's data) exceeds its level on average by 3-3.5%.

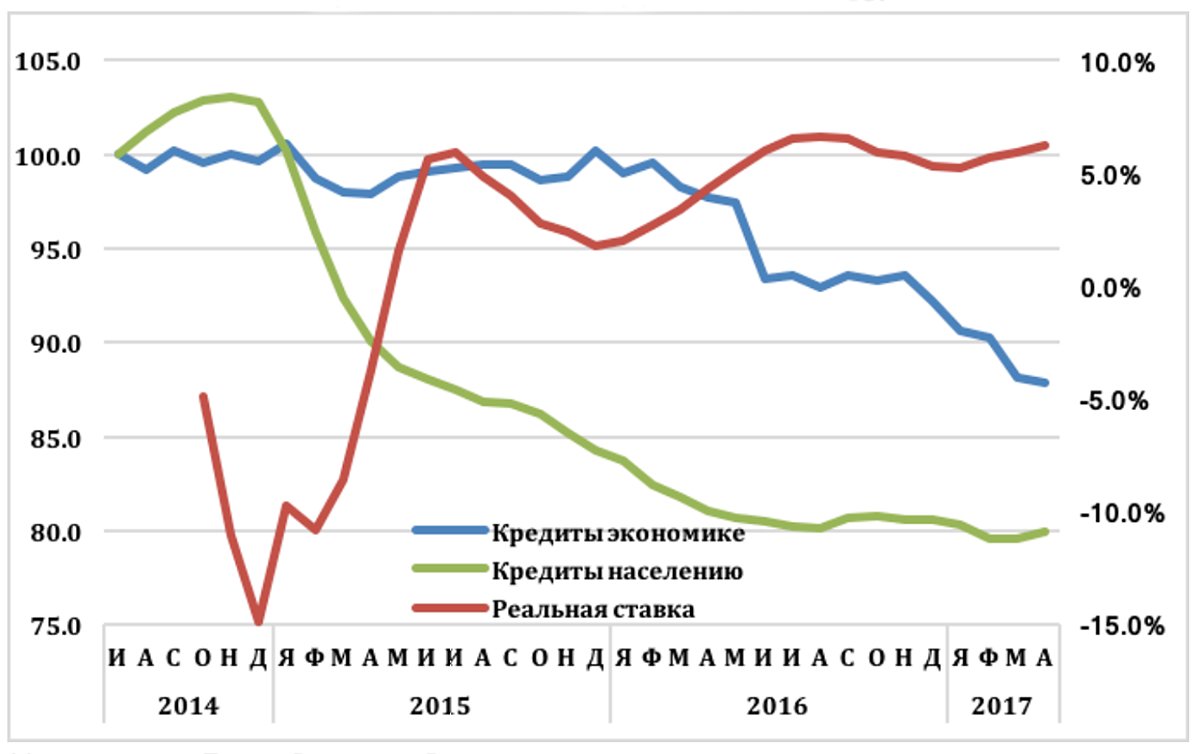

Chart 1. Real value of the key rate of the Bank of Russia (in percentages) and the trend of the real volume of credit in Russia (100 – July 2014), 2014-2017

Source: Bank of Russia, Rosstat

(To determine the real value of the key rate, I took the CPI for 6 months (3 months before and 3 months after the date; for May-June 2017 the CPI value is 0.2%). The real volume of credits is calculated as the sum of ruble credits deflated by the CPI, and the sum of foreign currency credits by accounting for their shares in the general volume of credits.

- It was stated that there would be no rapid lowering of the rate: the Bank of Russia has chosen the “small steps” tactic. As of today it is hard to say what the monetary authorities mean by “small”—0.25% or 0.5%? But one thing is clear: the lowering of the rate to the target level will continue for many more months. Such a pace of monetary policy normalization, in my opinion, is best summed up by the phrase: c’est pire qu’un crime, c’est une faute (“It is worse than a crime, it's a mistake.”) In the interview, justifying her decision, Nabiullina speaks about the hypothetical threat of a leap in inflation, which could require a raising of the rate. In my view, today’s Russian economy could see a leap in inflation due to two factors—a catastrophic crop failure or a sharp devaluation of the ruble. Nevertheless, I am not certain that in the first case a raising of the rate will help suppress price growth, and in the second case, raising the rate will be required irrespective of its level at that time.

- The Bank of Russia's goal to grow foreign currency reserves to $500 billion dollars was confirmed. However, Nabiullina said that the Bank of Russia might resume buying foreign currency after the market situation has stabilized, and intervene in such a way as not to influence the exchange rate of the ruble. These two statements have left me totally nonplussed . . . If we speak about market stability, then it would be hard to find a more favorable time than the last three months: export earnings grew faster than the demand of importers for foreign currency, and seasonality played a strong positive role—as a result, the exchange rate of the ruble has strengthened by 8.3% since the beginning of the year. What better situation could be expected? I don't understand. I also don't understand how purchases of foreign currency by the Bank of Russia could NOT influence the ruble's exchange rate—unless we are talking about miserly purchases of 10-20 million dollars a day, but in that case the goal of 500 billion dollars will always remain as far off as communism.

Either Be Happy, Or Cry

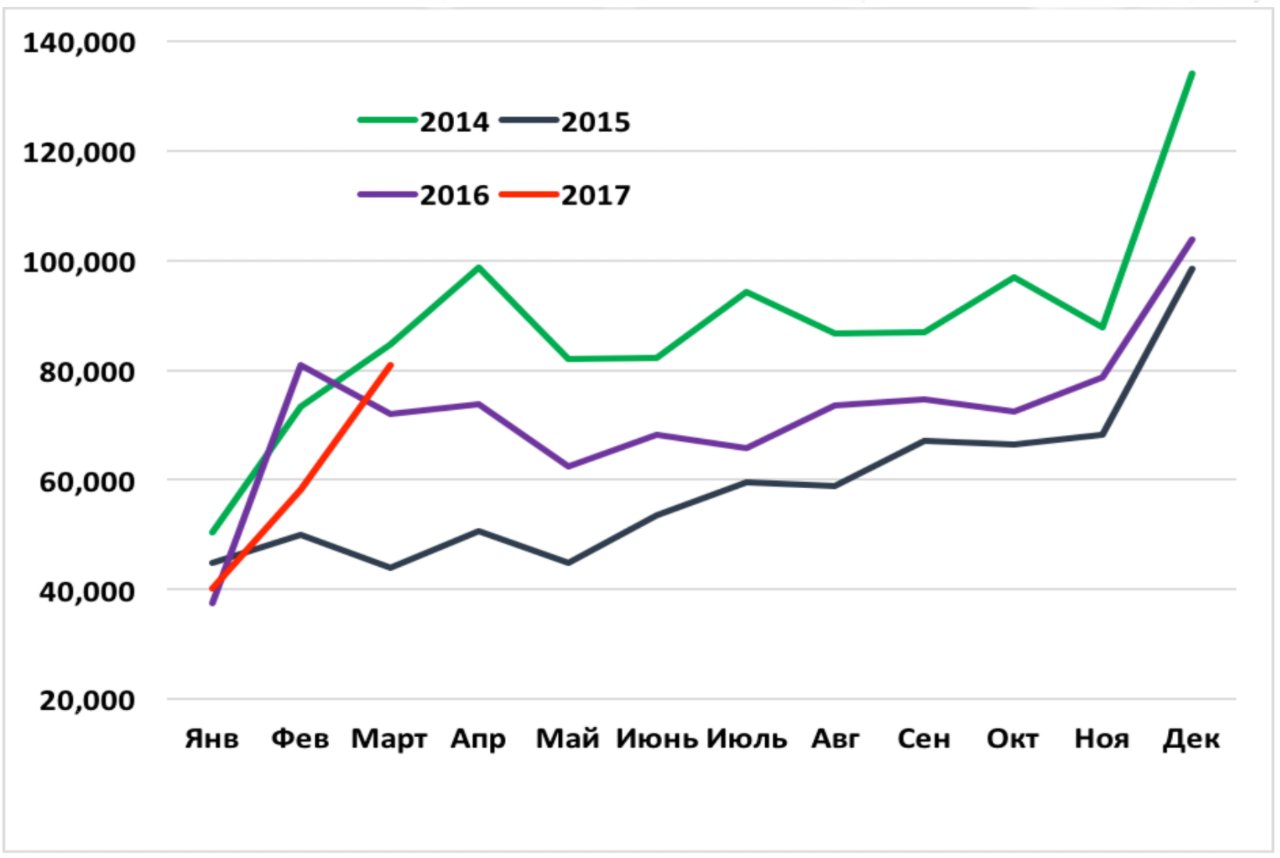

The March data on the issuance in Russia of new mortgage credits turned out to be more optimistic than those of one year ago, since for three months the volume of credits issued proved to be almost 6% lower than last year's amount. However, these data don't exactly inspire much enthusiasm; one has to admit that the number of Russian citizens ready to subject themselves to financial slavery over a period of many years (the average rate of the credits issued since the beginning of the year was 11.8%, with inflation at 4.3%), remains rather high.

Undoubtedly, the majority of them are hoping that in the future they'll be able to refinance today's expensive credit, but, judging by the Bank of Russia's behavior, that won't happen anytime soon.

Chart 2. Number of new mortgage credits issued in Russia, 2014-2017 (monthly, in units)

Source: Bank of Russia

Optimism is growing

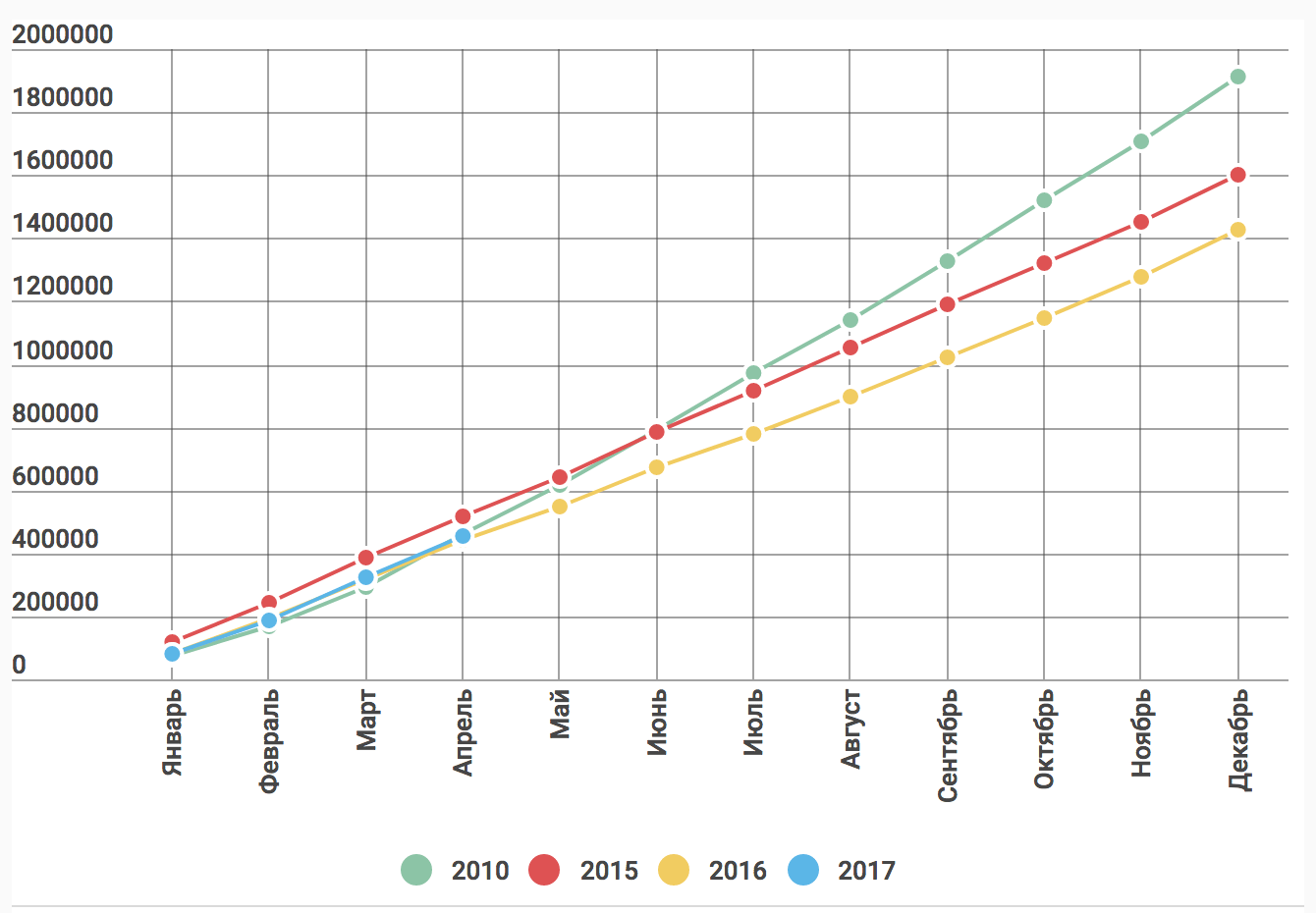

The car market in April supported the optimism born in March—sales of new vehicles again grew in comparison with last year, and by the end of the four months were 2.6% higher than a year ago, which saw the lowest level of sales for a decade.

Chart 3. Number of new passenger cars sold in Russia (cumulative total from the beginning of the year, in units), 2010, 2015-2017

Source: Association of European Business

It is true, however, that the results of the four-month period remain a little lower than the level in 2010 (to say nothing of the “fat” years of 2012-2014, when almost twice as many new cars were sold). But let's be optimistic, and continue to hope for a further improvement of the situation in this market sector.

The Market Versus the Cartel

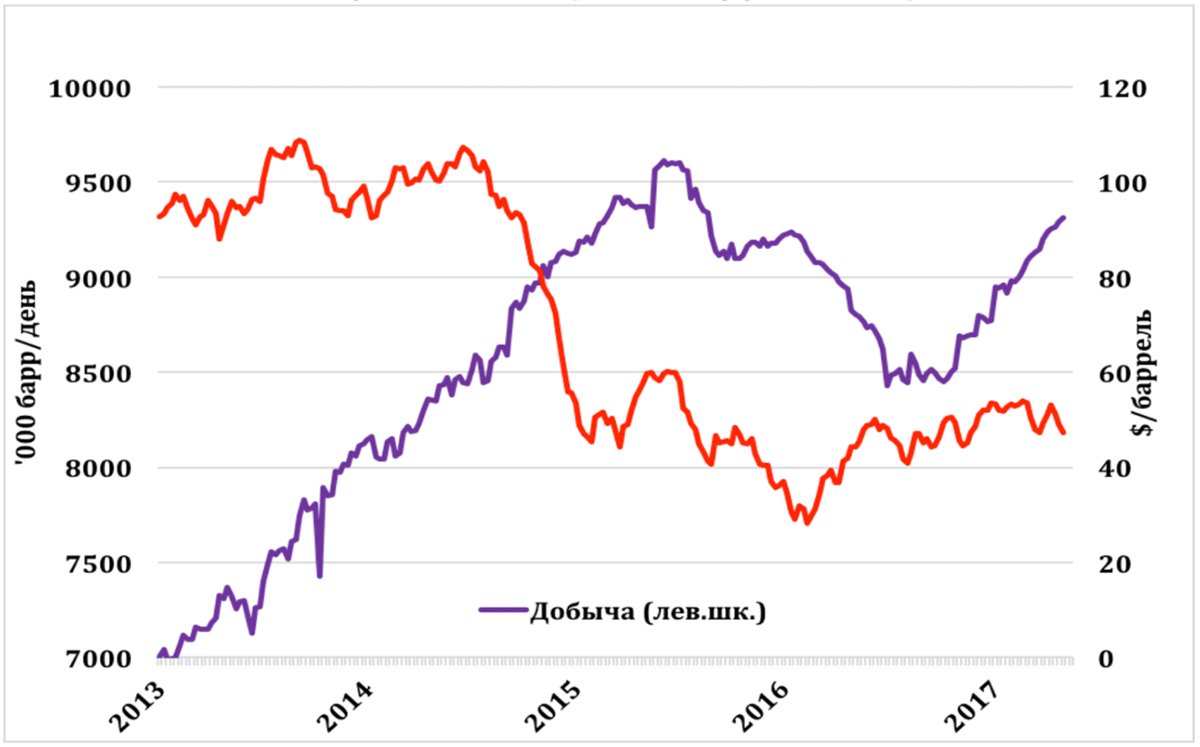

Oil is “our everything,” (to use a Russian idiom), so we impatiently await the decision of OPEC on a further reduction in oil production. This decision, taken at the end of last year, played a certain positive role (for oil producers). The price of “black gold” quickly rose by approximately $5 per barrel and . . . stopped in the range of $50-55 per barrel. The reasons for this are well known. On the one hand, the market still enjoys a glut of oil supply; on the other hand, American oil producers have used this “blessing” and rather quickly increased the volume of their daily production by 800,000 barrels. Although now the American oil industry has practically returned to the peak level from which it began to fall almost two years ago, it has noticeable resources for further increase of production. Drilling is taking place at a huge rate, with the number of wells that continue to be drilled growing by approximately 100 per month.

Chart 4. Price of WTI oil ($ per barrel) and oil production in the USA (thousands of barrels per day), 2013-2017

Source: Energy Information Administration

In such a situation the members of OPEC have another decision to make: to maintain the policy of cutting production, thereby leaving room for increasing oil production in the USA, or again to get into a production race. Most likely this time the present cap on production will be maintained and stricter limits shouldn't be expected—everyone wants to see how much oil production will increase in America. Meanwhile OPEC predicts that the limit on that is very close to the present level, which means that the members of the cartel need not fear that the USA will continue to “eat away” their share of the market.

So far, we can say that the American oil industry has a huge reserve of resilience: the decline in production began in the middle of 2015, almost a year after oil prices began to fall, and it ended only 20 weeks after oil prices hit bottom.

The English version of the original Russian article has been abridged and edited for clarity. You can access the full Russian version at openrussia.org.